Should you refinance your mortgage now that the Fed just cut rates? That’s the million-dollar question on everyone’s mind. With interest rates fluctuating like a rollercoaster, figuring out if refinancing is the right move can feel like navigating a financial maze. This guide cuts through the jargon, offering a clear-eyed look at the current interest rate environment, your personal mortgage situation, and the potential long-term financial implications of refinancing. We’ll break down the pros, cons, and costs, empowering you to make the smartest decision for your financial future.

We’ll explore different refinancing options, from rate-and-term refis to cash-out refis, and delve into the often-overlooked details like closing costs and prepayment penalties. Think of this as your ultimate cheat sheet for navigating the complex world of mortgage refinancing – because your financial peace of mind is worth it.

Current Interest Rate Environment

Source: themortgagereports.com

The Federal Reserve’s recent rate cut has sent ripples through the financial markets, impacting various borrowing costs, including mortgage rates. While a rate cut generally signals a more favorable borrowing environment, the actual impact on individual borrowers is complex and depends on several factors. Understanding the current landscape is crucial for anyone considering refinancing their mortgage.

The Fed’s rate cut aims to stimulate economic activity by making borrowing cheaper. This reduction in the federal funds rate, the target rate banks charge each other for overnight loans, typically influences other interest rates, including those for mortgages. However, the relationship isn’t always direct or immediate; mortgage rates are also affected by factors like investor demand for mortgage-backed securities and the overall economic outlook. While the rate cut might lead to lower mortgage rates, it’s not a guaranteed outcome.

Mortgage Rate Impact Following the Fed Rate Cut

The impact of the Fed’s rate cut on mortgage rates is not uniform and varies based on the type of mortgage (e.g., fixed-rate, adjustable-rate), the borrower’s credit score, and the lender’s pricing. Generally, a rate cut can lead to a decrease in mortgage rates, making refinancing more attractive. However, the magnitude of the decrease may not perfectly mirror the Fed’s rate cut. For instance, a 0.25% Fed rate cut might translate to a 0.125% to 0.20% decrease in mortgage rates, or even less depending on market conditions. It’s also important to note that lenders might not immediately adjust their rates after a Fed announcement, as they consider various market factors before making changes.

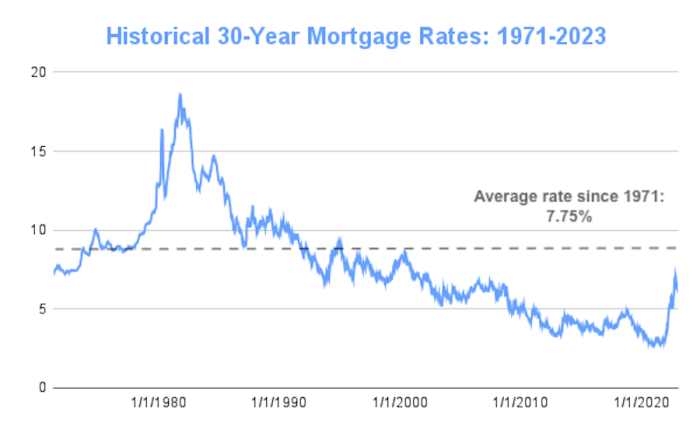

Historical Mortgage Rate Comparison

Comparing current mortgage rates to historical rates provides valuable context. Over the past few decades, mortgage rates have fluctuated significantly. For example, in the early 1980s, rates soared above 18%, while in recent years, they’ve been considerably lower, often in the 3-7% range. However, even within this lower range, significant variations occur based on economic conditions and market sentiment. Currently, rates are generally lower than they were a few years ago but might be slightly higher than the historical lows seen in 2020 and 2021. Checking a reliable financial website for historical mortgage rate data can provide a more precise comparison.

Current Mortgage Rate Table

Understanding the relationship between mortgage terms and interest rates is crucial for making informed refinancing decisions. The following table presents a hypothetical example of current rates for various mortgage terms. Note that these rates are illustrative and actual rates will vary depending on the lender, borrower profile, and prevailing market conditions.

| Mortgage Term (Years) | Interest Rate (%) | Monthly Payment (on $300,000 loan) | Total Interest Paid |

|---|---|---|---|

| 15 | 6.5 | $2,500 (approx.) | $120,000 (approx.) |

| 20 | 7.0 | $2,200 (approx.) | $192,000 (approx.) |

| 30 | 7.5 | $2,070 (approx.) | $325,000 (approx.) |

Your Current Mortgage Situation

Source: money.com

Before diving into whether refinancing makes sense for *you*, we need to take a hard look at your current mortgage. Understanding your existing loan’s details is crucial to evaluating potential savings and assessing the overall financial implications of refinancing. Ignoring this step could lead to regrettable decisions.

Let’s assume, for illustrative purposes, you have a 30-year fixed-rate mortgage with a 6% interest rate, a remaining balance of $200,000, and a monthly payment of approximately $1,200. This is a common scenario, allowing for a clear comparison with potential refinancing options. Remember to replace these figures with your own actual mortgage details.

Potential Savings from Refinancing

To illustrate potential savings, let’s say the new interest rate after the Fed rate cut is 4%. Using a mortgage calculator (easily found online), we can estimate the new monthly payment on a refinanced loan with the same $200,000 balance and a 30-year term. This calculation shows a potential monthly payment reduction to approximately $955. That’s a savings of $245 per month, or $2,940 annually! This is a significant amount that could be used for other financial goals. Keep in mind that this is a simplified example; your actual savings will depend on your specific loan terms, fees, and the final interest rate you qualify for.

Prepayment Penalties

It’s imperative to check the fine print of your current mortgage agreement. Many mortgages include prepayment penalties, which are fees charged if you pay off your loan early. These penalties can significantly impact the financial benefits of refinancing. Common penalty structures include a percentage of the remaining loan balance or a specific number of months’ worth of interest. For instance, a 2% prepayment penalty on our example loan would be $4,000. This needs to be factored into your decision-making process, potentially offsetting some or all of the short-term savings from a lower interest rate.

Pros and Cons of Refinancing

Understanding the potential advantages and disadvantages is critical to making an informed decision. Weighing these factors carefully is essential.

- Lower Monthly Payments: A lower interest rate translates directly to lower monthly payments, freeing up cash flow for other priorities.

- Reduced Total Interest Paid: Over the life of the loan, refinancing to a lower interest rate results in paying less total interest.

- Shorter Loan Term: Refinancing allows the possibility of shortening the loan term, leading to faster debt payoff.

- Potential for Cash Out: Depending on your home’s equity, you might be able to refinance for a higher amount, receiving cash back. However, this increases your overall debt.

- Closing Costs: Refinancing involves fees like appraisal costs, title insurance, and lender fees, which can eat into your savings.

- Prepayment Penalties: As discussed earlier, these fees can negate the benefits of refinancing.

- Interest Rate Risk: Rates could rise again after refinancing, negating the benefits of the initial rate reduction.

- Application Process: The process of applying and being approved for a new mortgage can be time-consuming and stressful.

Long-Term Financial Implications

Refinancing your mortgage can significantly impact your long-term financial health, extending beyond the immediate benefit of a lower monthly payment. A thorough analysis considering various factors is crucial to determine if refinancing aligns with your overall financial goals. While a lower interest rate might seem attractive, the total cost of homeownership over the life of the loan needs careful consideration.

Refinancing’s Effect on Monthly Mortgage Payments and Overall Homeownership Costs

A lower interest rate, achieved through refinancing, directly translates to a lower monthly mortgage payment. For example, consider a homeowner with a $300,000, 30-year mortgage at 7% interest. Their monthly payment might be around $2,000. Refinancing to a 5% interest rate could reduce their monthly payment to approximately $1,610, a significant saving of almost $400 per month. However, this reduction needs to be weighed against closing costs and the extended loan term. Refinancing to a longer term, even with a lower interest rate, could increase the total interest paid over the life of the loan, ultimately costing more in the long run. A shorter term will reduce the total interest paid but increase the monthly payment. The optimal choice depends on your financial priorities and risk tolerance.

Tax Implications of Refinancing

The tax implications of refinancing are primarily centered around the deduction of mortgage interest. If you itemize your taxes, you can deduct the interest paid on your mortgage. However, refinancing doesn’t automatically create a new deduction; it simply continues the existing deduction with the new loan terms. The amount of interest you can deduct will depend on the loan amount and interest rate. If you refinance to a larger loan amount, you may be able to deduct more interest, but this also increases your overall debt. Furthermore, points paid during refinancing are generally deductible over the life of the loan, which can provide some upfront tax savings. Consult a tax professional for personalized advice based on your specific circumstances.

Factors to Consider When Evaluating Long-Term Financial Effects

Before deciding to refinance, it’s vital to carefully assess several key factors that influence the long-term financial implications.

It’s important to consider these factors holistically. A seemingly advantageous lower interest rate might be offset by increased closing costs or a longer loan term. Careful calculation and professional advice are essential to make an informed decision.

- Closing Costs: These upfront costs can significantly impact the overall financial benefit of refinancing. They include appraisal fees, title insurance, lender fees, and more. These costs need to be factored into the total cost analysis to determine the break-even point – when the savings from the lower interest rate outweigh the closing costs.

- Loan Term: Extending the loan term reduces monthly payments but increases the total interest paid over the life of the loan. Shortening the term increases monthly payments but significantly reduces the total interest paid. The optimal choice depends on your financial priorities and risk tolerance.

- Interest Rate Difference: The magnitude of the interest rate reduction significantly impacts the financial benefits. A small reduction might not justify the closing costs, while a substantial reduction could yield significant long-term savings.

- Break-Even Point: This is the point in time when the cumulative savings from the lower monthly payment outweigh the closing costs. Calculating this point is crucial to determine the long-term financial viability of refinancing.

- Future Interest Rate Predictions: While impossible to predict with certainty, considering potential future interest rate movements can influence the decision. If rates are expected to fall further, waiting might be beneficial. Conversely, if rates are expected to rise, refinancing at the current lower rate might be advantageous.

Illustrative Examples

Let’s look at some real-world scenarios to illustrate when refinancing makes sense and when it doesn’t. Understanding these examples will help you make an informed decision about your own mortgage. Remember, every situation is unique, and professional advice is always recommended.

Refinancing can be a powerful tool to lower your monthly payments, shorten your loan term, or access your home equity. However, it’s crucial to weigh the potential benefits against the costs involved, such as closing costs and the potential for extending your loan term.

Scenario: Refinancing is Financially Advantageous

Imagine Sarah, a homeowner with a $300,000 mortgage at a 6% interest rate. She’s been making payments for five years and has built some equity. Interest rates have dropped to 4%. By refinancing to a 15-year mortgage at 4%, Sarah significantly reduces her monthly payments and saves a considerable amount of interest over the life of the loan. The lower interest rate outweighs the closing costs, making refinancing a financially sound decision. Her new lower monthly payment frees up cash flow for other financial goals.

Scenario: Refinancing is Not Financially Advantageous, Should you refinance your mortgage now that the fed just cut rates

Consider Mark, who has a $200,000 mortgage at a 5% interest rate. He’s only been making payments for two years. Interest rates have only dropped slightly to 4.75%. While a slight reduction in the interest rate is appealing, the closing costs associated with refinancing would nearly offset any savings he’d accrue over the remaining life of his loan. In this case, the short-term gains don’t justify the costs of refinancing. He’d be better off staying with his current mortgage.

Visual Representation of Refinancing Costs

Imagine a bar graph. The x-axis represents the years of the mortgage, and the y-axis represents the total cost (principal + interest). One bar represents the total cost of Mark’s existing mortgage (let’s say $350,000). A second, shorter bar represents the total cost of the same mortgage if he refinanced (let’s say $345,000). The difference between the two bars visually demonstrates the minimal savings from refinancing, highlighting the impact of closing costs. The visual clearly shows that the slight interest rate reduction doesn’t offset the cost of refinancing in Mark’s situation. A third bar, representing Sarah’s situation, would be significantly shorter than the first, showing substantial savings due to a larger interest rate reduction and a shorter loan term.

Questions to Ask a Mortgage Lender Before Refinancing

Before proceeding with refinancing, it’s vital to be well-informed. This section Artikels key questions to ask your lender to ensure transparency and a favorable outcome.

Asking these questions empowers you to make an informed decision. Don’t hesitate to seek clarification if anything is unclear.

- What are all the closing costs associated with refinancing?

- What is the Annual Percentage Rate (APR) for the new loan?

- What are the terms and conditions of the new loan, including prepayment penalties?

- What is the estimated monthly payment under the new loan?

- How long will the refinancing process take?

- What are my options if interest rates change during the refinancing process?

- What are the long-term financial implications of refinancing, considering both interest savings and closing costs?

Epilogue: Should You Refinance Your Mortgage Now That The Fed Just Cut Rates

Source: americandeposits.com

Ultimately, the decision of whether or not to refinance your mortgage after a Fed rate cut is deeply personal. It hinges on a careful evaluation of your current financial situation, your long-term goals, and a realistic assessment of the potential savings versus the associated costs. While lower rates present an enticing opportunity, a thorough understanding of your mortgage, the refinancing process, and the potential long-term implications is crucial. Don’t rush into a decision; arm yourself with the knowledge you need to make the best choice for your unique circumstances.