High yield bonds savings ideas as fed weighs rate cut – sounds like a financial rollercoaster, right? With the Fed potentially slashing interest rates, the landscape for high-yield bond investments is shifting. This means both exciting opportunities and serious risks. We’re diving deep into how this move could impact your savings strategy, exploring the potential rewards and the pitfalls to avoid. Get ready to navigate the thrilling world of high-yield bonds – it’s time to make your money work smarter, not harder.

This article breaks down the complexities of high-yield bonds, explaining what they are, who issues them, and why their yields fluctuate. We’ll analyze how a Fed rate cut could influence investor sentiment and the potential impact on your portfolio. We’ll also compare high-yield bonds to other savings options, helping you decide if they’re the right fit for your risk tolerance and financial goals. Prepare for a clear-eyed look at the potential upsides and downsides, with practical strategies to help you make informed decisions.

High Yield Bonds

High-yield bonds, also known as junk bonds, offer the allure of higher returns compared to investment-grade bonds. However, this increased yield comes with a significantly higher risk of default. Understanding the nuances of these bonds is crucial for investors considering adding them to their portfolio.

High-Yield Bond Characteristics

High-yield bonds are debt securities issued by companies with lower credit ratings, typically below investment grade (Ba1/BB+ or lower). These ratings reflect a higher probability of default. Typical issuers include companies with high levels of debt, those undergoing financial restructuring, or emerging market corporations. The lower credit rating directly translates to a higher yield offered to compensate investors for the increased risk.

Factors Influencing High-Yield Bond Yields

Several factors interplay to determine the yield on high-yield bonds. The most prominent is the issuer’s creditworthiness; a company with a weaker credit rating will need to offer a higher yield to attract investors. Market interest rates also play a crucial role; rising interest rates generally lead to lower bond prices and higher yields, while falling rates have the opposite effect. Economic conditions, investor sentiment, and industry-specific factors further influence the yield. For example, during economic downturns, the default risk of high-yield bonds increases, leading to higher yields. Conversely, during periods of economic expansion, the demand for higher-yielding bonds can push yields down.

Risk Profile Comparison

High-yield bonds carry substantially more risk than investment-grade bonds. Investment-grade bonds, with ratings of Baa3/BBB- or higher, have a much lower probability of default. Compared to other asset classes like equities (stocks), high-yield bonds offer a different risk-reward profile. While equities offer the potential for higher returns, they also carry significantly higher volatility and risk of principal loss. High-yield bonds sit somewhere in between, offering a higher return potential than investment-grade bonds but with greater risk than equities, particularly during economic downturns. A diversified portfolio may include a small allocation to high-yield bonds for those seeking higher yield, but the overall portfolio’s risk tolerance must be carefully considered.

Examples of High-Yield Bond Investments

The suitability of high-yield bonds depends heavily on individual risk tolerance and investment goals. A conservative investor might allocate a small portion of their portfolio to high-yield bonds with relatively strong credit ratings within the BB range, focusing on established companies with a history of consistent performance. Conversely, a more aggressive investor with a higher risk tolerance might consider bonds with lower ratings (B or below) from companies operating in rapidly growing sectors, accepting higher risk for potentially higher returns. It is crucial to remember that past performance is not indicative of future results and that even seemingly secure high-yield bonds can default. Therefore, thorough due diligence and professional financial advice are essential before investing in high-yield bonds. For instance, a hypothetical example could be comparing two bonds: one from a well-established telecommunications company with a BB rating and another from a smaller, rapidly growing biotech firm with a B rating. The telecom bond would likely offer a lower yield but with less risk, while the biotech bond would offer a higher yield but with significantly higher default risk.

The Federal Reserve’s Rate Cut and its Impact on High-Yield Bonds

The Federal Reserve’s decision to cut interest rates is a significant event with ripple effects across the financial landscape, particularly impacting the high-yield bond market. Understanding the reasons behind a rate cut and its potential consequences is crucial for investors navigating this complex terrain. A rate cut typically signals the central bank’s assessment of a slowing economy or a need to stimulate growth.

The anticipated effect on the economy is multifaceted. Lower interest rates aim to make borrowing cheaper for businesses and consumers, encouraging investment and spending. This, in theory, leads to increased economic activity and job creation. However, rate cuts also carry risks, such as fueling inflation if the economy overheats.

Investor Sentiment and High-Yield Bonds Following a Rate Cut

A Fed rate cut can significantly influence investor sentiment towards high-yield bonds. Lower rates generally make riskier assets, like high-yield bonds, more attractive. This is because the reduced cost of borrowing makes it easier for companies to service their debt, reducing the risk of default. Conversely, lower rates also decrease the yield advantage of high-yield bonds compared to safer investments like government bonds. This trade-off requires careful consideration by investors. Historically, periods of rate cuts have often been associated with increased demand for high-yield bonds, leading to price appreciation.

Risks and Opportunities in High-Yield Bonds During Rate Cuts

Investing in high-yield bonds during a period of rate cuts presents both opportunities and risks. One key opportunity lies in the potential for capital appreciation as investor demand increases. However, the reduced yield spread compared to other asset classes needs to be carefully weighed. Furthermore, the economic conditions that necessitate a rate cut can also increase the risk of defaults among lower-rated companies, especially if the economic slowdown is more severe than anticipated. Therefore, careful due diligence and a diversified portfolio are essential.

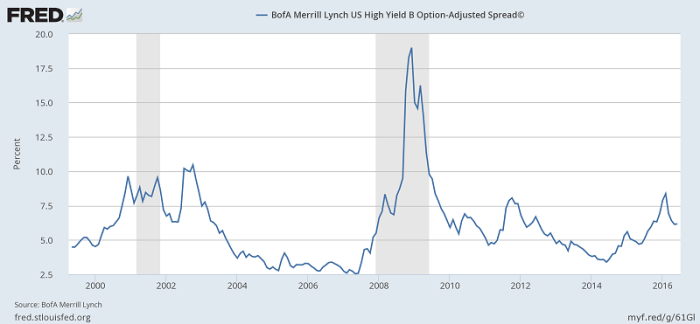

Historical Examples of Fed Rate Cuts and High-Yield Bond Performance

The impact of Fed rate cuts on high-yield bonds has varied historically depending on the overall economic context. For instance, during the 2008 financial crisis, the Fed implemented aggressive rate cuts, but the high-yield market still experienced significant losses due to the widespread economic downturn and credit crunch. Conversely, in periods of milder economic slowdowns accompanied by rate cuts, the high-yield bond market has often shown resilience and even experienced positive returns, as seen in certain instances during the early 2000s. It’s crucial to analyze the specific economic environment and the reasons behind the rate cut to better predict its effect on high-yield bonds. The 1990s, for example, showed a generally positive correlation between rate cuts and high-yield performance, although each instance must be analyzed individually. The specifics of each economic climate and the broader market conditions are key to interpreting the relationship between Fed action and high-yield returns.

High-Yield Bond Investment Strategies

Source: thismatter.com

Navigating the world of high-yield bonds requires a strategic approach, especially considering the fluctuating influence of Federal Reserve rate decisions. Understanding various investment strategies is crucial for maximizing returns while mitigating risks. This section explores different approaches to incorporating high-yield bonds into your portfolio, catering to varying risk tolerances and market outlooks.

Diversified High-Yield Bond Portfolio Design

A well-structured high-yield bond portfolio shouldn’t be a monolithic investment. Diversification across issuers, industries, and maturities is key to reducing overall portfolio volatility. For example, a balanced portfolio might include bonds from diverse sectors like energy, healthcare, and technology, with a mix of short-term, intermediate-term, and long-term maturities. This strategy aims to reduce the impact of a single issuer defaulting or a specific sector underperforming. Consider also incorporating different credit ratings within the high-yield spectrum, acknowledging the trade-off between higher yields and increased default risk. A well-diversified portfolio might allocate 30% to bonds rated BB+, 40% to BB, and 30% to B, for example, reflecting a carefully considered risk appetite. This diversification aims to capitalize on higher yields while acknowledging the higher risk of lower-rated bonds. During periods of economic uncertainty, like those potentially triggered by Fed rate cuts, a more conservative approach might be warranted, favoring higher-rated high-yield bonds and shorter maturities.

Investment Plan for a Risk-Averse Investor, High yield bonds savings ideas as fed weighs rate cut

A risk-averse investor seeking high-yield exposure should prioritize capital preservation. A suitable strategy might involve allocating a smaller portion of their portfolio (e.g., 10-15%) to high-yield bonds, complementing it with investments in safer assets like government bonds or high-quality corporate bonds. Focusing on investment-grade high-yield bonds (those closer to the BB+ rating) is also crucial. Dollar-cost averaging (discussed later) would further mitigate risk by spreading investments over time rather than making a lump-sum investment at a potentially unfavorable market moment. Regular monitoring of the portfolio’s performance and credit ratings of the held bonds is also necessary. This cautious approach accepts a lower potential return in exchange for significantly reduced risk. A real-life example would be a retiree who prioritizes income stability over aggressive growth.

Comparison of Active and Passive High-Yield Bond Management

Active management involves a fund manager actively selecting individual bonds based on their assessment of market conditions and individual issuer prospects. This approach seeks to outperform a benchmark index, but it comes with higher fees. Passive management, on the other hand, involves investing in an index fund that tracks a specific high-yield bond index. This strategy offers lower fees and broader diversification, mirroring the index’s performance. The choice depends on the investor’s belief in the manager’s skill and their willingness to pay for active management. Historical performance data can be compared to assess the potential advantages of each approach, although past performance doesn’t guarantee future results. For example, some studies suggest that actively managed high-yield bond funds have not consistently outperformed their passive counterparts over the long term.

Dollar-Cost Averaging in High-Yield Bond Investments

Dollar-cost averaging (DCA) involves investing a fixed amount of money at regular intervals, regardless of the market price. This strategy reduces the risk of investing a lump sum at a market peak. For example, an investor might invest $1,000 per month in a high-yield bond fund. When prices are low, more bonds are purchased; when prices are high, fewer bonds are purchased. Over time, the average cost per bond is likely to be lower than if the entire sum were invested at a single point in time. This reduces the impact of market volatility and helps to smooth out returns. This strategy is particularly useful for investors who are uncomfortable timing the market and prefer a systematic approach to investing. The effectiveness of DCA is enhanced when applied over a longer investment horizon.

Alternative Savings Ideas in a Low-Interest Rate Environment: High Yield Bonds Savings Ideas As Fed Weighs Rate Cut

Source: corporatefinanceinstitute.com

The Federal Reserve’s potential rate cuts, while potentially beneficial for certain sectors, leave savers searching for alternatives to traditional accounts offering meager returns. High-yield bonds offer one avenue, but a diversified approach considering risk tolerance is crucial. This section explores other savings vehicles and investment options that might be suitable alternatives depending on your individual financial goals and risk appetite. We’ll compare these options to high-yield bonds, highlighting their relative strengths and weaknesses.

High-yield bonds, while potentially offering higher returns than traditional savings accounts, carry inherent risks. The possibility of default by the issuer is a key consideration. Therefore, understanding alternative investment strategies with similar or lower risk profiles is vital for informed decision-making.

Certificates of Deposit (CDs) and Money Market Accounts Compared to High-Yield Bonds

CDs and money market accounts offer a degree of safety and liquidity not always present in high-yield bonds. CDs provide a fixed interest rate for a specified term, guaranteeing a known return, albeit often a lower one compared to high-yield bonds. Money market accounts, while offering slightly higher flexibility than CDs, generally offer lower returns still. The trade-off is clear: higher potential returns in high-yield bonds come with higher risk of default; CDs and money market accounts prioritize capital preservation over maximizing returns. For example, a typical CD might offer a 4% annual percentage yield (APY) while a high-yield bond could offer 7%, but with the increased risk of non-payment. The choice depends on your individual risk tolerance and time horizon.

Alternative Investment Options with Similar Risk Profiles to High-Yield Bonds

Several investment options offer risk profiles comparable to high-yield bonds, though each comes with its own set of considerations. Real Estate Investment Trusts (REITs) and peer-to-peer lending are two examples. Diversification across these options can help mitigate overall portfolio risk. It is important to conduct thorough due diligence before investing in any of these alternatives.

Real Estate Investment Trusts (REITs) as an Alternative

REITs are companies that own or finance income-producing real estate. They offer a way to invest in real estate without directly owning property. REITs often pay high dividends, which can be comparable to the yields offered by high-yield bonds. However, REIT returns can be sensitive to interest rate changes and fluctuations in the real estate market. For example, a decline in property values could negatively impact the value of your REIT investments. Furthermore, the dividend payouts from REITs are not guaranteed and can be reduced or eliminated depending on the performance of the underlying real estate assets.

Peer-to-Peer Lending as a High-Yield Alternative

Peer-to-peer (P2P) lending platforms connect borrowers directly with lenders, cutting out traditional financial intermediaries. This can lead to higher potential returns for lenders compared to traditional savings accounts. However, P2P lending carries significant risks, including the possibility of borrower default and the lack of regulatory oversight in some jurisdictions. A borrower’s failure to repay a loan can result in a complete loss of your investment. Furthermore, the lack of comprehensive regulatory frameworks in some P2P lending markets means that investor protection might be limited. Therefore, careful selection of borrowers and platforms is essential. Diversifying your P2P lending portfolio across multiple borrowers and platforms can help mitigate some of the inherent risks.

Illustrating High-Yield Bond Performance

Source: federalreserve.gov

High-yield bonds, also known as junk bonds, offer the potential for higher returns than investment-grade bonds, but they also carry significantly more risk. Understanding their historical performance across different market cycles is crucial for any investor considering adding them to their portfolio. This section will explore both successful and unsuccessful scenarios, highlighting the factors that contribute to their varied performance.

Analyzing historical data provides valuable insights into the potential rewards and risks associated with high-yield bonds. While past performance doesn’t guarantee future results, it can illuminate typical return patterns and volatility levels. The following table illustrates a hypothetical example based on a representative high-yield bond index, showcasing the interplay between yield, return, and risk over time.

High-Yield Bond Index Performance (Hypothetical Example)

| Year | Yield (%) | Return (%) | Standard Deviation (%) |

|---|---|---|---|

| 2018 | 6.5 | 4.2 | 12.1 |

| 2019 | 7.0 | 9.8 | 8.5 |

| 2020 | 5.2 | -2.1 | 15.7 |

| 2021 | 4.8 | 11.5 | 9.2 |

| 2022 | 8.0 | -5.9 | 14.3 |

Note: This table presents a hypothetical example and does not represent the performance of any specific index. Standard deviation is used here as a simple measure of risk. More sophisticated risk metrics might be employed in a real-world analysis.

Exceptional High-Yield Bond Portfolio Performance

A scenario where a high-yield bond portfolio performs exceptionally well might involve a period of strong economic growth coupled with low inflation. Imagine a period like the late 1990s, where robust corporate earnings fueled investor confidence. A portfolio manager who strategically invested in high-yield bonds issued by companies in rapidly expanding sectors (e.g., technology) could have reaped substantial returns. Careful selection of issuers with strong fundamentals and a focus on bonds with shorter maturities would further mitigate risk and enhance returns during this period of economic optimism. The combination of strong economic growth and careful issuer selection contributed significantly to the portfolio’s success.

Underperforming High-Yield Bond Portfolio

Conversely, an underperforming high-yield bond portfolio could be attributed to a period of economic recession or market downturn, such as the 2008 financial crisis. During such times, many high-yield issuers face financial distress, leading to defaults and significant losses for bondholders. A portfolio heavily concentrated in bonds issued by companies in struggling sectors (e.g., real estate or financial services during the 2008 crisis) would have likely underperformed dramatically. Furthermore, a lack of diversification and a reliance on longer-maturity bonds would have amplified the negative impact of defaults and market volatility. The confluence of economic downturn, poor issuer selection, and unfavorable portfolio construction contributed to the portfolio’s underperformance.

Final Summary

So, are high-yield bonds the answer to your savings prayers in this era of potential rate cuts? Maybe, maybe not. The truth is, there’s no one-size-fits-all answer. The key takeaway here is thorough research and understanding your own risk tolerance. While high-yield bonds offer the potential for higher returns, they also come with significantly higher risk. By carefully weighing the pros and cons, diversifying your portfolio, and understanding the current economic climate, you can navigate this complex financial landscape and potentially boost your savings game. Remember, knowledge is power – and in the world of finance, that power translates to smarter, more profitable decisions.