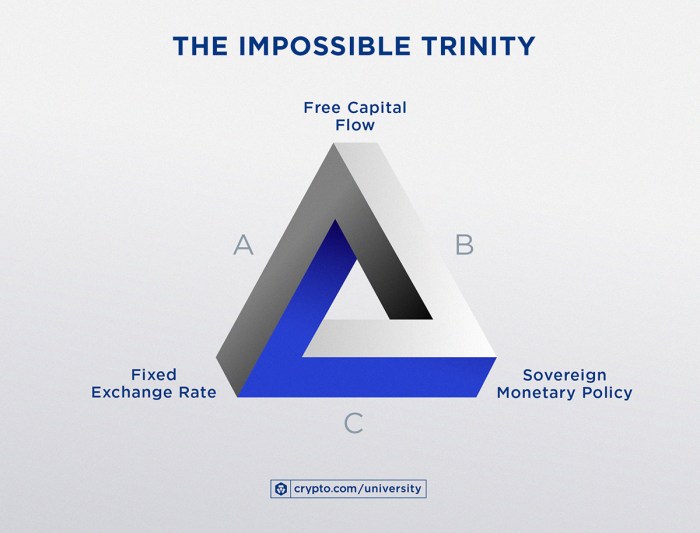

The impossible trinity why countries cannot have it all – The Impossible Trinity: Why Countries Cannot Have It All – it sounds like a riddle, right? But this economic concept, also known as the Mundell-Fleming Trilemma, is a hard reality for nations worldwide. It boils down to a simple yet crucial choice: a country can only realistically pursue two out of three key policy goals: a fixed exchange rate, free capital movement, and an independent monetary policy. Choosing one means sacrificing another, leading to complex trade-offs with significant economic consequences.

This seemingly simple choice has far-reaching implications. Maintaining a fixed exchange rate might offer stability but could stifle economic growth if it limits monetary policy flexibility. Conversely, prioritizing an independent monetary policy, crucial for managing inflation and unemployment, might necessitate sacrificing a fixed exchange rate or restricting capital flows. This article delves into the intricacies of this trilemma, exploring the historical context, the trade-offs involved, and case studies of nations grappling with these critical decisions.

Introduction to the Impossible Trinity: The Impossible Trinity Why Countries Cannot Have It All

The Impossible Trinity, also known as the Mundell-Fleming Trilemma, is a fundamental concept in international finance that highlights the inherent trade-offs nations face when managing their economies. It essentially boils down to this: a country can only pursue two out of three key macroeconomic policy goals simultaneously. Trying to achieve all three is, well, impossible. Understanding this trilemma is crucial for comprehending the choices governments make regarding their currency, capital flows, and monetary policy.

The three policy goals at the heart of the Impossible Trinity are interconnected and often conflicting. These are: a fixed exchange rate, free capital movement, and an independent monetary policy. A fixed exchange rate means the government pegs its currency to another currency (like the US dollar) or a basket of currencies, maintaining a relatively stable exchange rate. Free capital movement implies that capital (money) can flow freely into and out of the country without government restrictions. Finally, an independent monetary policy allows a central bank to set interest rates and control the money supply to achieve domestic economic goals, such as controlling inflation or boosting employment.

The Three Policy Goals Explained

Each of the three policy goals represents a distinct approach to economic management. A fixed exchange rate offers stability and predictability for businesses engaged in international trade, reducing exchange rate risk. Free capital movement promotes investment and economic growth by allowing for efficient allocation of capital across borders. An independent monetary policy provides flexibility to address domestic economic shocks and pursue specific inflation or unemployment targets. However, attempting to simultaneously maintain all three creates inherent contradictions.

Historical Overview and Modern Relevance

The Impossible Trinity’s theoretical foundations were laid by Robert Mundell and Marcus Fleming in the 1960s, reflecting the growing interconnectedness of global economies. Their work provided a framework for understanding the challenges faced by countries in managing their exchange rates, capital flows, and monetary policies. Historically, countries have often chosen to prioritize two of the three goals, depending on their specific economic circumstances and priorities. For instance, countries with pegged exchange rates (like those in the Eurozone) sacrifice independent monetary policy. Conversely, countries with freely floating exchange rates (like the US) give up control over the exchange rate but retain independent monetary policy and free capital movement.

The Impossible Trinity remains highly relevant today in a globalized world characterized by significant capital mobility. The ongoing debate surrounding monetary policy responses to economic crises, the impact of capital controls, and the desirability of fixed versus floating exchange rates all underscore the enduring significance of this economic trilemma. The choice a nation makes reflects its unique economic priorities and vulnerabilities in a complex and interconnected global landscape. Understanding these trade-offs is key to analyzing the economic strategies of nations worldwide.

The Trade-offs Involved

Source: economicshelp.org

The Impossible Trinity forces nations to make difficult choices. Attempting to achieve all three goals – a fixed exchange rate, free capital movement, and independent monetary policy – is akin to trying to square a circle. Each policy goal offers distinct advantages but also carries significant drawbacks. Understanding these trade-offs is crucial for policymakers in navigating the complex landscape of international finance.

The core challenge lies in the inherent conflict between these three policy objectives. Maintaining a fixed exchange rate requires limiting the ability to adjust interest rates independently, as these rate adjustments can impact currency values. Similarly, allowing free capital movement means that monetary policy actions can be quickly undermined by capital flows moving in or out of the country. Choosing any two goals necessitates sacrificing the third, leading to specific economic consequences depending on the choice made.

Fixed Exchange Rate and Free Capital Movement: Sacrificing Monetary Policy Independence

Choosing a fixed exchange rate and free capital movement forces a country to relinquish control over its monetary policy. The central bank loses the ability to use interest rates to manage inflation, unemployment, or economic growth. Interest rates must align with those of the country to which the currency is pegged, effectively surrendering control over domestic monetary conditions. This can be particularly problematic during economic shocks. For instance, if a country experiences a recession while maintaining a fixed exchange rate with a stronger economy, its central bank cannot lower interest rates to stimulate growth without risking a currency devaluation. The country is locked into the monetary policy dictated by its pegged currency’s home country.

Fixed Exchange Rate and Independent Monetary Policy: Sacrificing Free Capital Movement

When a nation prioritizes a fixed exchange rate and an independent monetary policy, it must restrict capital mobility. This usually involves implementing capital controls, such as limitations on foreign investment or restrictions on the movement of funds across borders. While this allows the central bank to manage interest rates to achieve domestic economic goals, it comes at the cost of hindering foreign investment, reducing access to international capital markets, and potentially limiting economic growth. China, for example, has historically implemented capital controls to maintain a degree of control over its currency and monetary policy.

Free Capital Movement and Independent Monetary Policy: Sacrificing a Fixed Exchange Rate

Countries opting for free capital movement and independent monetary policy allow their exchange rate to float freely. This means the currency’s value is determined by market forces of supply and demand. The central bank retains control over its monetary policy tools, allowing it to respond to domestic economic conditions. However, this comes with the risk of exchange rate volatility. Fluctuations in the exchange rate can impact the prices of imports and exports, potentially leading to inflation or deflation. The United States, with its floating exchange rate and independent monetary policy, exemplifies this approach. The value of the dollar can fluctuate significantly based on various global economic factors, influencing the price of imported goods and affecting the competitiveness of American exports. While this provides flexibility, it also introduces uncertainty into the economy.

Fixed Exchange Rate Regimes and Their Implications

Maintaining a fixed exchange rate, a cornerstone of monetary policy for many nations, involves a delicate balancing act. It means a country’s currency is pegged to another currency or a basket of currencies at a specific rate. This seemingly simple act has profound implications for a nation’s economic health and stability.

A fixed exchange rate offers several perceived advantages: price stability, reduced exchange rate risk for businesses engaging in international trade, and a potential anchor for inflation expectations. However, the path to achieving and maintaining this stability is fraught with challenges.

Mechanisms for Maintaining a Fixed Exchange Rate

Countries employ various mechanisms to maintain a fixed exchange rate. The most common involve direct intervention in the foreign exchange market by the central bank. If the domestic currency starts to depreciate against the pegged currency, the central bank buys its own currency using its foreign exchange reserves, increasing demand and thus supporting the exchange rate. Conversely, if the domestic currency appreciates too much, the central bank sells its own currency, increasing supply and preventing excessive appreciation. This requires the central bank to hold substantial foreign currency reserves, a significant commitment of resources. Other mechanisms include adjusting interest rates – higher rates attract foreign capital, increasing demand for the domestic currency – and implementing capital controls, restricting the flow of capital in and out of the country.

Challenges in Defending a Fixed Exchange Rate

Defending a fixed exchange rate under pressure can be incredibly difficult. Speculative attacks, where investors bet against the currency, can quickly deplete a country’s foreign exchange reserves. A large capital outflow, perhaps triggered by economic instability or loss of confidence in the government, can overwhelm even the most robust intervention efforts. Maintaining a fixed rate often necessitates sacrificing monetary policy independence. The central bank’s ability to adjust interest rates to address domestic economic conditions is limited by the need to maintain the exchange rate peg. This can lead to situations where the country’s monetary policy is inappropriate for its internal economic needs. Furthermore, maintaining a fixed exchange rate might mask underlying economic imbalances, postponing necessary adjustments and potentially leading to a more severe crisis later.

Examples of Fixed Exchange Rate Regimes

The success or failure of a fixed exchange rate regime depends heavily on a variety of factors, including the strength of the country’s economy, the credibility of its government, and the size of its foreign exchange reserves.

| Country | Regime Type | Success/Failure | Reasons |

|---|---|---|---|

| Hong Kong | Hong Kong dollar pegged to the US dollar | Success | Strong economic fundamentals, large foreign exchange reserves, and a credible monetary authority. The link has been maintained for decades. |

| Argentina (various periods) | Peso pegged to the US dollar (various attempts) | Failure (multiple instances) | Economic mismanagement, high inflation, and speculative attacks ultimately led to the collapse of several peso pegs. Lack of structural reforms and fiscal discipline contributed to these failures. |

| Denmark | Danish krone pegged to the euro | Success | Strong economic performance and commitment to maintaining the peg. The central bank actively intervenes to maintain the exchange rate within a narrow band. |

| East Asian Countries (1997-98 Crisis) | Various pegs (e.g., Thai baht, Indonesian rupiah) | Failure | Underlying economic weaknesses, including large current account deficits and excessive borrowing in foreign currencies, were exposed by speculative attacks. The fixed exchange rate regimes ultimately collapsed, triggering a regional financial crisis. |

Free Capital Movement and its Effects

The ability of capital to flow freely across borders is a defining characteristic of globalization, impacting everything from national interest rates to economic growth. While offering significant advantages, unrestricted capital movement also presents considerable challenges, particularly within the context of the Impossible Trinity. Understanding these advantages and disadvantages is crucial for policymakers grappling with macroeconomic stability.

Free capital movement, in essence, means money – investments, loans, and financial assets – can move easily between countries without significant government restrictions. This facilitates international trade and investment, allowing countries to access a wider pool of funds for development and growth. However, this freedom comes at a cost, particularly when a country is attempting to maintain a fixed exchange rate.

Advantages of Unrestricted Capital Flows

Unrestricted capital flows provide several benefits. Firstly, it enhances economic efficiency by allowing capital to flow to its most productive uses, regardless of geographical location. A country with abundant savings can invest in a country with high-return investment opportunities, boosting overall global productivity. Secondly, it promotes competition and innovation, as businesses can access a broader range of funding sources and technologies. Increased competition can lead to lower prices and better quality goods and services for consumers. Finally, it increases liquidity in financial markets, allowing for smoother price discovery and risk management. This improved liquidity can also stabilize exchange rates in a floating regime.

Disadvantages of Unrestricted Capital Flows

Conversely, unrestricted capital flows also carry significant risks. One major concern is the volatility they can introduce into a country’s economy. Sudden surges of capital inflows can inflate asset prices, creating bubbles that eventually burst, leading to financial crises. Similarly, rapid capital outflows can trigger currency depreciations and economic instability. Furthermore, unrestricted capital flows can exacerbate income inequality, as the benefits often accrue disproportionately to those who own capital, potentially leading to social unrest. Another disadvantage is the potential for increased susceptibility to external shocks, as a country’s economy becomes more integrated with the global financial system.

The Role of Capital Controls in Managing the Impossible Trinity

Capital controls, essentially restrictions on the movement of capital across borders, are often employed as a tool to manage the trade-offs inherent in the Impossible Trinity. By limiting capital inflows or outflows, countries can regain control over their monetary policy and exchange rate regime. For example, a country aiming to maintain a fixed exchange rate might implement capital controls to prevent speculative attacks that could destabilize the currency. However, capital controls are not without their own drawbacks. They can distort markets, reduce investment, and limit access to international finance. The effectiveness of capital controls also depends heavily on their design and enforcement. A poorly designed control regime can be easily circumvented, rendering it ineffective.

Impact of Capital Flows on Different Types of Economies, The impossible trinity why countries cannot have it all

The impact of capital flows differs significantly between developed and developing economies. Developed economies, with robust financial institutions and regulatory frameworks, are generally better equipped to manage the risks associated with unrestricted capital flows. They have more diversified financial markets and can better absorb shocks. Developing economies, on the other hand, are often more vulnerable to the volatility of capital flows. Their financial systems are often less developed, making them more susceptible to financial crises. For instance, a sudden surge in capital inflows can lead to overvaluation of the currency, hurting export competitiveness. Conversely, a sudden outflow can lead to a currency crisis and a sharp contraction in economic activity. Many developing countries, therefore, employ capital controls as a means of managing these risks and protecting their economies from external shocks. The East Asian financial crisis of 1997-98 serves as a stark reminder of the devastating consequences that uncontrolled capital flows can have on emerging markets.

Independent Monetary Policy and its Limitations

Source: crypto.com

A nation’s ability to independently manage its monetary policy is a cornerstone of economic sovereignty. This control allows governments to fine-tune economic levers, influencing inflation and unemployment to achieve desired growth and stability. However, this power isn’t absolute, especially within the context of the Impossible Trinity. The pursuit of independent monetary policy often necessitates trade-offs, particularly when a country aims to simultaneously maintain a fixed exchange rate and free capital movement.

Independent monetary policy is crucial for managing inflation and unemployment because it allows central banks to adjust interest rates and money supply to counteract economic fluctuations. Raising interest rates, for example, can curb inflation by making borrowing more expensive and reducing consumer spending. Conversely, lowering interest rates can stimulate economic activity during a recession by encouraging investment and consumption. The effectiveness of these tools depends on a multitude of factors, including the responsiveness of the economy to monetary policy changes and the overall global economic environment.

The Conflict Between Independent Monetary Policy and Fixed Exchange Rates

Maintaining a fixed exchange rate requires a country to keep its currency’s value stable against another currency or a basket of currencies. This often involves intervention in the foreign exchange market – buying or selling its own currency to maintain the desired exchange rate. However, this intervention directly clashes with independent monetary policy. If a country’s central bank wants to lower interest rates to boost the economy, it may lead to a decrease in demand for its currency, putting downward pressure on the exchange rate. To maintain the fixed rate, the central bank would need to intervene by buying its own currency, potentially limiting the effectiveness of the initial interest rate cut. Conversely, if the central bank raises interest rates to combat inflation, this may attract foreign capital, increasing demand for the domestic currency and potentially leading to an appreciation of the currency beyond the desired fixed rate. The central bank would then have to sell its currency to prevent appreciation, thereby offsetting the intended effect of the interest rate hike. This constant balancing act severely limits the central bank’s ability to use monetary policy for domestic economic goals.

Examples of Monetary Policy Adjustments

Several countries have navigated this trade-off in different ways. For instance, during the European Monetary System (EMS), many European countries pegged their currencies to the German mark. This meant their central banks had limited control over their monetary policies, needing to align their interest rates with Germany’s to maintain the fixed exchange rate. This sometimes led to periods of economic hardship for countries whose economies required different monetary policies. Another example is China, which has maintained a managed exchange rate regime for a considerable period. While China has some degree of monetary policy independence, it often needs to consider the impact of its monetary policy decisions on the exchange rate, carefully balancing domestic economic needs with the goal of maintaining a relatively stable exchange rate against the US dollar. These examples highlight the complexities involved in balancing the objectives of monetary policy independence, exchange rate stability, and free capital movement.

Case Studies

The Impossible Trinity, while a theoretical concept, plays out in real-world economies with fascinating consequences. Examining how different nations have navigated this trilemma provides valuable insights into the trade-offs inherent in macroeconomic policy. By prioritizing one aspect of the trinity, countries implicitly accept limitations in the other two. Let’s delve into some compelling examples.

Case Study: China – Managed Exchange Rate and Capital Controls

China’s economic strategy for decades has involved maintaining a relatively stable, albeit managed, exchange rate for its currency, the Renminbi (RMB). This policy choice has prioritized exchange rate stability and, to a degree, independent monetary policy. To achieve this, China has implemented significant capital controls, limiting the free flow of capital in and out of the country.

- Country: China

- Chosen Policies: Managed exchange rate, capital controls, relatively independent monetary policy (with limitations).

- Outcomes: Sustained economic growth, but with limitations on financial market development and potential for capital flight if controls are loosened too quickly. The managed exchange rate has allowed for the gradual appreciation of the RMB, while capital controls have helped maintain domestic financial stability and reduce vulnerability to external shocks. However, this system has also led to concerns about the RMB’s undervaluation and the potential for future volatility.

This case study highlights the trade-off between exchange rate stability and free capital movement. China’s success demonstrates that a managed exchange rate, coupled with effective capital controls, can support economic growth, but at the cost of limiting financial market integration and potentially hindering long-term financial development.

Case Study: The Eurozone – Fixed Exchange Rate and Monetary Union

The Eurozone represents a unique case study, characterized by a fixed exchange rate (the Euro) amongst its member states and a shared monetary policy conducted by the European Central Bank (ECB). This arrangement effectively sacrifices independent monetary policy for each individual member country. While capital flows freely within the Eurozone, the lack of individual monetary control presents challenges.

- Country: Eurozone (e.g., Germany, France, Greece)

- Chosen Policies: Fixed exchange rate (Euro), free capital movement, shared monetary policy.

- Outcomes: Reduced transaction costs within the Eurozone, increased trade and economic integration. However, the lack of individual monetary policy flexibility has led to economic imbalances and difficulties responding to country-specific economic shocks. The Eurozone crisis of 2008-2012 demonstrated the challenges of managing a monetary union with diverse economic structures and vulnerabilities. Countries like Greece faced significant economic hardship because they lacked the ability to devalue their currency to boost exports or adjust interest rates to stimulate their economy.

The Eurozone experience demonstrates the significant challenges of a monetary union, particularly when member states have differing economic structures and vulnerabilities. The prioritization of a fixed exchange rate and free capital movement comes at the cost of losing individual monetary policy independence, leading to potential economic instability.

Case Study: United States – Floating Exchange Rate and Independent Monetary Policy

The United States operates under a floating exchange rate regime, allowing its currency (the US dollar) to fluctuate freely against other currencies. This system prioritizes both independent monetary policy and free capital movement.

- Country: United States

- Chosen Policies: Floating exchange rate, free capital movement, independent monetary policy.

- Outcomes: Flexibility in responding to economic shocks through monetary policy adjustments. The ability to attract foreign investment due to free capital movement. However, the exchange rate is subject to significant volatility, potentially impacting trade and investment flows. This volatility is a direct result of the interaction of supply and demand in the foreign exchange market, driven by various factors such as interest rate differentials, economic growth, and political uncertainty.

The US example highlights that while having independent monetary policy and free capital movement offers flexibility and attracts investment, it also comes with the inherent risk of exchange rate volatility. This volatility can create uncertainty for businesses and investors, underscoring the trade-offs inherent in this policy mix.

The Impossible Trinity in a Globalized World

Source: numerade.com

Globalization, the increasing interconnectedness of economies through trade, capital flows, and information exchange, has profoundly reshaped the landscape of international finance. This interconnectedness significantly impacts the feasibility and implications of the Impossible Trinity, forcing nations to constantly re-evaluate their policy priorities in a rapidly changing global environment. The traditional trade-offs become even more complex in this context, demanding sophisticated strategies to navigate the challenges of maintaining macroeconomic stability.

Globalization intensifies the challenges of managing the Impossible Trinity. Increased capital mobility, a defining feature of globalization, makes it significantly harder for countries to maintain fixed exchange rates or independent monetary policies. Simultaneously, the interconnectedness of global markets amplifies the impact of shocks, making it crucial for nations to coordinate their policies and respond effectively to global economic events. The free flow of capital across borders allows for rapid adjustments to interest rate differentials, making it difficult for countries to control their own monetary policy without experiencing substantial capital inflows or outflows.

Increased Capital Mobility and Exchange Rate Volatility

The ease with which capital flows across borders in a globalized world intensifies the pressure on exchange rates. A country attempting to maintain a fixed exchange rate while simultaneously pursuing an independent monetary policy faces significant challenges. Any divergence between domestic and international interest rates will lead to substantial capital flows, potentially overwhelming the country’s ability to defend its exchange rate peg. For instance, if a country’s interest rates are higher than those in the global market, it might attract large capital inflows, putting upward pressure on its currency. To maintain the peg, the central bank would need to intervene by buying foreign currency and selling its own, potentially depleting its foreign exchange reserves. Conversely, lower interest rates can lead to significant capital outflows, causing downward pressure on the currency.

The Challenge of Coordinated Monetary Policy

In a globalized world, the actions of one country’s central bank can have ripple effects across the globe. The need for coordinated monetary policies becomes crucial to mitigate the risk of destabilizing international financial markets. However, achieving such coordination can be difficult, given the diverse economic conditions and policy priorities of different nations. The 2008 global financial crisis highlighted the limitations of uncoordinated monetary policies, with the crisis originating in the US quickly spreading to other countries due to the interconnectedness of financial markets. A coordinated response, while eventually implemented, was hampered by differing national interests and political considerations.

Technological Advancements and Fintech

The rise of fintech and other technological advancements further complicates the Impossible Trinity. These technologies facilitate faster and more efficient cross-border transactions, making capital mobility even more fluid and challenging to control. Cryptocurrencies and decentralized finance (DeFi) platforms offer alternative financial systems that operate outside the traditional regulatory frameworks, potentially undermining a country’s ability to manage its monetary policy and exchange rate. The use of blockchain technology, for example, allows for instantaneous and borderless transactions, making it difficult for governments to monitor and regulate capital flows effectively. This necessitates new regulatory frameworks and international cooperation to navigate the complexities of this evolving financial landscape.

Illustrative Representation of Global Finance Interconnectedness

Imagine a three-circle Venn diagram. Each circle represents one of the three policy goals: fixed exchange rate, free capital movement, and independent monetary policy. The area where all three circles overlap represents the “impossible” space – a state that cannot be sustainably maintained. However, globalization significantly expands the outer regions of each circle. The free capital movement circle, for example, is substantially larger, reflecting the increased ease and speed of international capital flows. The interconnectedness is depicted by lines linking the three circles, illustrating how a policy decision in one area inevitably impacts the others. For instance, a line connecting the “free capital movement” and “fixed exchange rate” circles indicates that large capital flows can destabilize a fixed exchange rate regime. Similarly, lines linking “independent monetary policy” and the other two circles highlight the tension between maintaining independent monetary policy and either a fixed exchange rate or unrestricted capital movement in a globalized world. The diagram visually represents the heightened complexity and trade-offs inherent in managing the Impossible Trinity in the context of a globally integrated financial system.

Last Recap

Navigating the Impossible Trinity is a constant balancing act for policymakers. There’s no one-size-fits-all solution; the optimal approach depends heavily on a nation’s specific economic circumstances and priorities. Understanding the trade-offs involved – between stability, flexibility, and open markets – is crucial for formulating effective economic policies. The Impossible Trinity isn’t just an abstract economic theory; it’s a practical challenge shaping the economic landscape of nations globally, forcing tough choices with lasting repercussions.