Is it worth getting a high yield savings account before the next fed meeting – Is it worth getting a high-yield savings account before the next Fed meeting? That’s the million-dollar question (well, maybe not a million, but a decent chunk of change!), especially with interest rates fluctuating like a rollercoaster. This isn’t your grandma’s savings account; we’re talking about maximizing your returns in a potentially volatile market. Let’s dive into the potential upsides and downsides of jumping on the high-yield bandwagon before the Fed makes its next move.

The Federal Reserve’s decisions directly impact interest rates, influencing how much your savings earn. Understanding the current rate environment, projected changes, and alternative investment options is crucial for making an informed decision. We’ll break down the risks and rewards, helping you decide if a high-yield savings account aligns with your financial goals and risk tolerance before the next Fed meeting.

Current Interest Rate Environment

Source: cbsnewsstatic.com

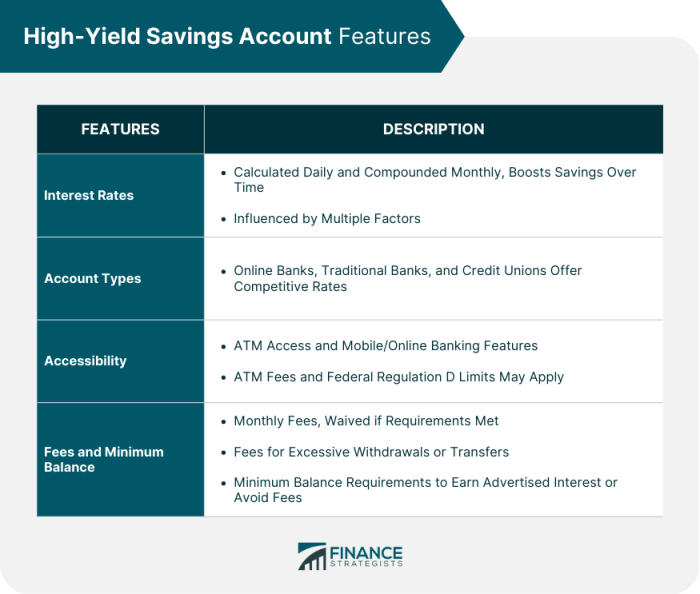

The current interest rate environment is a dynamic landscape shaped by the Federal Reserve’s (Fed) monetary policy decisions. Understanding this environment is crucial for anyone considering a high-yield savings account, as the Fed’s actions directly influence the returns you can expect. The interplay between the federal funds rate and high-yield savings account interest rates is a key factor to consider before the next Fed meeting.

The federal funds rate, the target rate that the Fed sets for overnight lending between banks, is a cornerstone of monetary policy. When the Fed raises this rate, it becomes more expensive for banks to borrow money. This increased cost is typically passed on to consumers through higher interest rates on various financial products, including high-yield savings accounts. Conversely, a reduction in the federal funds rate usually leads to lower interest rates on these accounts. Currently, the federal funds rate is [Insert Current Federal Funds Rate and Date – Source needed here, e.g., Federal Reserve website]. This rate significantly influences the interest rates offered by banks on high-yield savings accounts, though the exact impact varies depending on the bank’s individual policies and market conditions.

The Historical Relationship Between Fed Meetings and Savings Account Interest Rates

Historically, there’s a strong correlation between Fed meetings and subsequent changes in savings account interest rates. Following a Fed rate hike, banks typically adjust their offerings on high-yield savings accounts upwards, albeit often with a lag. This lag can range from a few weeks to several months, depending on market dynamics and individual bank strategies. For example, after the significant rate hikes in [Insert Year and Period of Rate Hikes – Source needed], many high-yield savings accounts saw their annual percentage yields (APYs) increase substantially within a few months. Conversely, periods of rate cuts have historically seen a decline in APYs offered on high-yield savings accounts, though again, the timing and magnitude of these changes vary. Analyzing past Fed meeting announcements and the subsequent changes in savings account rates provides valuable insight into potential future trends.

Comparison of High-Yield Savings Account Yields with Other Short-Term Investment Options, Is it worth getting a high yield savings account before the next fed meeting

High-yield savings accounts are not the only game in town when it comes to short-term investments. While they offer the convenience of easy access and FDIC insurance (up to $250,000 per depositor, per insured bank), their returns might not always be the highest compared to other options. For example, short-term certificates of deposit (CDs) often offer slightly higher interest rates but come with penalties for early withdrawal. Money market accounts (MMAs) also present a competitive alternative, although their yields can fluctuate more than those of high-yield savings accounts. The best option depends on individual circumstances, risk tolerance, and investment goals. A detailed comparison of current APYs for high-yield savings accounts, CDs, and MMAs would be needed to make an informed decision. Consider the trade-off between liquidity and potential returns when evaluating these alternatives. For instance, a high-yield savings account provides easy access to your funds, while a CD may lock your money away for a specified term.

Projected Fed Rate Changes

Predicting the Federal Reserve’s next move on interest rates is a complex game of economic chess, with several factors influencing the outcome. While no one can definitively say what the Fed will do, analyzing current economic indicators and historical trends allows us to Artikel a range of plausible scenarios. Understanding these potential scenarios is crucial for anyone considering a high-yield savings account, as the interest rates offered are directly impacted by the Fed’s decisions.

The Fed’s primary mandate is to maintain price stability and maximum employment. To achieve this, they utilize monetary policy tools, primarily adjusting the federal funds rate – the target rate banks charge each other for overnight loans. Changes in the federal funds rate ripple through the entire financial system, influencing borrowing costs for consumers and businesses, ultimately affecting inflation and employment. A rate hike aims to cool down an overheating economy by making borrowing more expensive, while a rate cut stimulates economic activity by making borrowing cheaper.

Potential Fed Rate Scenarios and Their Impact

Several factors will weigh heavily on the Fed’s decision at the next meeting. Inflation data, particularly the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) index, will be closely scrutinized. A persistent decline in inflation towards the Fed’s 2% target would likely support a pause or even a rate cut. Conversely, stubbornly high inflation, perhaps fueled by strong consumer spending or persistent supply chain issues, might lead to another rate hike. Employment data, including the unemployment rate and wage growth, will also play a significant role. A strong labor market with low unemployment and rising wages could fuel inflationary pressures, prompting the Fed to act cautiously. Finally, global economic conditions and geopolitical events can indirectly influence the Fed’s decisions. For example, global recessionary fears might lead the Fed to be more cautious about raising rates.

| Scenario | Fed Rate Change | Impact on HYSA Rate | Overall Investment Recommendation |

|---|---|---|---|

| Scenario 1: Aggressive Rate Hike | 0.25% – 0.50% increase | High-yield savings account rates likely increase, but potentially lag behind the Fed rate change. | Maintain or increase HYSA holdings for higher returns, but diversify investments. |

| Scenario 2: Pause in Rate Hikes | No change | HYSA rates may plateau or experience a slight decrease depending on market conditions. | Maintain current HYSA holdings; explore other investment options based on risk tolerance. |

| Scenario 3: Rate Cut | 0.25% – 0.50% decrease | HYSA rates will likely decrease significantly. | Consider shifting some funds to other investment vehicles offering better returns, depending on the market situation and your risk appetite. May consider keeping some funds in HYSA for liquidity. |

Risks and Rewards of High-Yield Savings Accounts

So, you’re eyeing those juicy interest rates on high-yield savings accounts (HYSA)? Smart move, especially in this fluctuating interest rate environment. But before you dive headfirst, let’s unpack the good, the bad, and the potentially ugly. High-yield savings accounts aren’t a get-rich-quick scheme, but they can be a valuable tool in your financial arsenal if used strategically.

High-yield savings accounts offer a compelling blend of accessibility and potentially higher returns compared to traditional savings accounts. However, understanding the inherent risks is crucial for making informed decisions. Let’s delve into the details.

Interest Rate Risk

Interest rates are dynamic; they’re not static numbers etched in stone. What this means for your HYSA is that the high interest rate you’re enjoying today might not be around tomorrow. Banks adjust their rates based on various economic factors, including the Federal Reserve’s actions. A decrease in the federal funds rate will likely lead to a decrease in the interest rate offered on your HYSA. This isn’t necessarily a bad thing, but it’s crucial to understand that your returns aren’t guaranteed to remain consistently high. For example, imagine you locked in a 4% APY in early 2023. If interest rates fall, your returns could drop significantly the following year, even if your balance remains the same.

FDIC Insurance Limitations

The Federal Deposit Insurance Corporation (FDIC) insures deposits in banks up to $250,000 per depositor, per insured bank, for each account ownership category. This means that if a bank fails, the FDIC will protect your money up to that limit. However, if you have more than $250,000 in a single HYSA, or spread across multiple accounts at the same bank, you could face potential losses exceeding the FDIC coverage. Therefore, spreading your deposits across multiple FDIC-insured institutions might be a prudent strategy to mitigate this risk. This is especially important for high-net-worth individuals.

Advantages of High-Yield Savings Accounts

High-yield savings accounts offer several advantages over traditional savings accounts. The most obvious is the higher interest rate, leading to potentially greater returns on your savings. This allows your money to work harder for you, helping you reach your financial goals faster, whether it’s a down payment on a house or building an emergency fund. Furthermore, access to your funds is typically easy and convenient, unlike some investments that require a longer lock-in period or involve complex procedures to withdraw funds.

Opportunity Cost of High-Yield Savings Accounts

While a HYSA provides a relatively safe place for your money to grow, it’s essential to consider the opportunity cost. This refers to the potential return you could have earned by investing your money elsewhere. While the risk is lower in a HYSA, the potential for higher returns from investments like stocks or bonds is also higher, but with significantly more risk. The decision of whether to keep your money in a HYSA versus investing it in higher-return assets depends on your individual risk tolerance, financial goals, and time horizon. For example, someone saving for retirement in 20 years might be more comfortable taking on more risk with their investments, while someone saving for a down payment in two years might prefer the stability of a HYSA.

Alternative Investment Strategies

So, you’ve weighed the pros and cons of high-yield savings accounts. But are they the *only* game in town for your short-term cash? Absolutely not! Let’s explore some alternatives and see how they stack up. Understanding the nuances of each option is crucial for making the best financial decision for your unique situation.

Comparison of Short-Term Investment Options

Choosing the right short-term investment depends on your risk tolerance, time horizon, and financial goals. Below, we compare high-yield savings accounts with money market accounts (MMAs) and certificates of deposit (CDs), highlighting key differences.

| Investment Type | Interest Rate | Risk Level | Liquidity |

|---|---|---|---|

| High-Yield Savings Account | Variable, generally higher than traditional savings accounts. Currently averaging around 4-5% (as of October 26, 2023, this is subject to change). | Very Low | High; access funds readily. |

| Money Market Account (MMA) | Variable, often slightly higher than HYSA, but may have minimum balance requirements. Similar average range to HYSA. | Very Low | High, but may have limitations on withdrawals compared to HYSAs. |

| Certificate of Deposit (CD) | Fixed, generally higher than HYSAs and MMAs, but with penalties for early withdrawal. Rates vary widely based on term length and institution. | Low | Low; funds are locked in for a specific term. |

Return on Investment Calculations

Let’s illustrate potential returns. Assume you invest $10,000.

For a High-Yield Savings Account with a 4% annual interest rate, your return after one year would be:

$10,000 * 0.04 = $400

For a CD with a 5% annual interest rate and a one-year term, your return would be the same:

$10,000 * 0.05 = $500

However, a CD’s higher return comes with the trade-off of reduced liquidity. Early withdrawal penalties can significantly eat into your earnings. For example, if you withdrew your money from a 5% CD after six months, you might forfeit several months of interest. The exact penalty would vary by financial institution. MMAs would yield results similar to HYSAs in this scenario, varying slightly depending on the institution and prevailing interest rates.

Individual Financial Circumstances

Source: financestrategists.com

Deciding whether a high-yield savings account (HYSA) is right for you before the next Fed meeting hinges entirely on your unique financial picture. It’s not a one-size-fits-all answer, and rushing into a decision without careful consideration could be costly. Let’s examine how your personal situation plays a role.

Let’s imagine Sarah, a 30-year-old marketing professional, is contemplating opening a HYSA. She’s saving for a down payment on a condo in two years and currently has $15,000 in a low-yield savings account. Her risk tolerance is low, preferring security over potentially higher returns. This scenario highlights how individual circumstances dictate the suitability of a HYSA.

Sarah’s Savings and Financial Goals

Sarah’s existing savings and her clearly defined goal (a down payment) are crucial factors. The $15,000 represents a significant portion of her down payment target, and she needs a safe place to park it while it grows. A HYSA, with its FDIC insurance (up to $250,000 per depositor, per insured bank, for each account ownership category) offers that security. The relatively short timeframe (two years) makes the potential for higher returns from riskier investments less appealing. Her goal is capital preservation, not maximizing returns.

Sarah’s Risk Tolerance and the HYSA Decision

Sarah’s low risk tolerance perfectly aligns with the nature of a HYSA. While HYSA interest rates fluctuate, they remain relatively stable compared to investments like stocks or bonds. The FDIC insurance further mitigates risk. For Sarah, the peace of mind knowing her savings are safe and insured outweighs the potential for slightly higher returns from more volatile options. Choosing a HYSA is a rational choice given her circumstances.

Opening a HYSA and Transferring Funds

The process of opening a HYSA is generally straightforward. Most banks and online financial institutions offer them. Sarah would need to compare interest rates, fees, and account minimums across several providers to find the best fit. Once she chooses an institution, she’ll typically need to provide personal information, such as her Social Security number and address, for verification. Transferring funds from her existing low-yield account can often be done online through an automated transfer or by initiating a wire transfer. Some institutions may require a minimum deposit to open the account. The entire process usually takes only a few business days.

Illustrative Example

Source: citizenside.com

Let’s visualize how your savings could grow in a high-yield savings account over a year, considering different interest rate scenarios. Understanding these projections helps you make informed decisions about your financial planning, especially in the face of potential Fed rate changes. We’ll use a simple visual representation to illustrate this.

Imagine a line graph. The horizontal axis represents the months of the year (January to December). The vertical axis represents the total savings balance. We’ll plot three lines on this graph, each representing a different interest rate scenario: a conservative scenario (low interest rate), a moderate scenario (medium interest rate), and an optimistic scenario (high interest rate).

Projected Savings Growth Under Different Interest Rate Scenarios

The conservative scenario line would show a relatively slow, steady upward climb. This reflects a low interest rate, perhaps around 3% annually. The moderate scenario line would show a steeper incline, representing a moderate interest rate, say, 4.5% annually. Finally, the optimistic scenario line would show the most dramatic upward trend, reflecting a higher interest rate, perhaps 6% annually. All three lines start at the same point, representing your initial savings amount. The difference between the lines at the end of the year clearly illustrates the impact of varying interest rates on your savings growth. For instance, starting with $10,000, the conservative scenario might yield around $300 in interest, the moderate scenario around $450, and the optimistic scenario around $600. This simple visualization makes the compounding effect of interest rates readily apparent.

Final Conclusion: Is It Worth Getting A High Yield Savings Account Before The Next Fed Meeting

So, is a high-yield savings account a smart move before the next Fed meeting? The answer, like most financial decisions, depends on your unique circumstances. Weighing the potential for higher returns against the risks of interest rate fluctuations is key. Consider your financial goals, risk tolerance, and the opportunity cost of keeping your money in a savings account versus other investments. Ultimately, doing your research and understanding your options empowers you to make the best decision for your financial future. Don’t just react to the market; strategically plan your savings strategy.