Colorado Property Tax Reform: The Centennial State is grappling with a property tax system that’s, let’s just say, *interesting*. From wildly varying rates across counties to the complexities of assessment appeals, navigating Colorado’s property taxes can feel like scaling a mountain in flip-flops. This deep dive explores the current system, the arguments for and against reform, and what potential changes could mean for homeowners, renters, and businesses alike. We’ll unpack the proposed reforms, examine their potential impacts, and even peek into alternative funding mechanisms for public services. Get ready to ditch the flip-flops and lace up your hiking boots – this is going to be a journey.

This isn’t just about numbers and spreadsheets; it’s about the very fabric of Colorado communities. How do we balance fairness, affordability, and the essential funding of vital public services? We’ll examine the potential economic consequences, the impact on different demographics, and even look at successful (and unsuccessful) reforms in other states. Prepare for a no-holds-barred exploration of one of Colorado’s most pressing issues.

Current State of Colorado Property Taxes

Source: coloradohardmoney.com

Colorado’s property tax system, while seemingly straightforward, presents a complex landscape for homeowners and businesses alike. Understanding its intricacies is crucial for navigating the financial implications of owning property in the Centennial State. This section delves into the assessment methods, tax rates, and appeal processes that shape the property tax burden across Colorado’s diverse counties and municipalities.

Colorado Property Tax System Overview

Colorado’s property tax system relies on a combination of state-mandated guidelines and locally determined rates. The state constitution limits the amount of property taxes that can be levied, but individual counties and municipalities have considerable leeway in setting their own rates within those limits. Property is assessed based on its market value, a figure determined through a process that considers recent sales of comparable properties. This assessment forms the basis for calculating the annual property tax bill. Different types of property (residential, commercial, agricultural, etc.) are subject to varying assessment methods and tax rates, reflecting their differing contributions to the local tax base.

Types of Property Taxes in Colorado

Several types of property taxes are levied in Colorado, each serving a specific purpose. These include general property taxes, which fund essential local government services such as schools, public safety, and infrastructure. Specific districts, like school districts or special districts (e.g., water districts, fire protection districts), may also levy their own property taxes to support their operations. These taxes are added to the general property tax bill, resulting in a potentially significant overall tax burden. Finally, there are often mill levies imposed at the local level, further adding to the complexity of the system. Understanding the breakdown of these different levies is crucial for understanding the full cost of property ownership.

Property Tax Assessment and Appeals Process

The process of property tax assessment begins with county assessors evaluating properties based on market value. Assessors utilize various data points, including recent sales of similar properties, to determine a property’s assessed value. Property owners have the right to appeal their assessed valuation if they believe it’s inaccurate or unfairly high. This appeal process involves submitting evidence, such as recent appraisals or comparable sales data, to the county’s Board of Equalization. If the appeal is unsuccessful at the county level, it can be further appealed to the Colorado Board of Assessment Appeals. This multi-stage process ensures that property owners have recourse if they feel their tax assessment is unjust.

Examples of Property Tax Calculations in Colorado Counties

Calculating property taxes in Colorado involves several steps. First, the assessed value of the property is determined. Then, the tax rate, expressed in mills (one mill equals one-tenth of one cent per dollar of assessed valuation), is applied. The mill levy is the sum of the rates for all taxing entities (county, school district, etc.). For example, a property assessed at $300,000 in a county with a combined mill levy of 50 mills would have an annual property tax of $15,000 ($300,000 x 0.050). However, this is a simplified example. Actual calculations can be significantly more complex due to various exemptions, credits, and other factors specific to each county and taxing entity. The differences in assessment practices and mill levies across counties lead to significant variations in property tax burdens.

Property Tax Rates Across Major Colorado Cities

| City | Effective Tax Rate (Mills) | Median Home Value (Estimate) | Approximate Annual Property Tax |

|---|---|---|---|

| Denver | ~55 | ~$550,000 | ~$30,250 |

| Boulder | ~60 | ~$700,000 | ~$42,000 |

| Colorado Springs | ~48 | ~$400,000 | ~$19,200 |

| Fort Collins | ~52 | ~$500,000 | ~$26,000 |

*Note: These are estimates based on publicly available data and may vary depending on specific property characteristics and taxing districts. Actual rates and values should be verified with local authorities.*

Arguments for Property Tax Reform in Colorado

Source: futurecdn.net

Colorado’s property tax system, while seemingly straightforward, presents significant challenges for residents and the state’s economic health. Reform is urgently needed to address escalating tax burdens, promote equitable distribution of wealth, and foster a more robust and inclusive economy. This section Artikels compelling arguments supporting a comprehensive overhaul of the current system.

Economic Benefits of Property Tax Reform

A modernized property tax system can unlock significant economic benefits for Colorado. Lower property taxes, particularly for lower- and middle-income homeowners, would free up disposable income, stimulating local economies through increased consumer spending. This increased spending would ripple through the economy, benefiting businesses and creating jobs. Furthermore, a more predictable and equitable tax system can attract new businesses and residents, boosting investment and economic growth. This contrasts with the current system, where unpredictable assessments can deter investment and create uncertainty for both businesses and individuals. For example, a study by the [insert credible source here, e.g., Colorado Fiscal Institute] could illustrate the potential economic multipliers associated with tax relief. The study might show how every dollar of tax reduction leads to X dollars of increased economic activity.

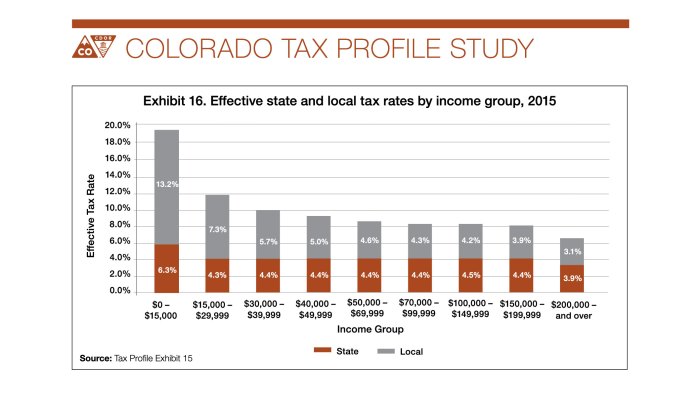

Impact of Property Taxes on Different Demographics, Colorado property tax reform

The current property tax system disproportionately affects certain demographic groups in Colorado. Senior citizens on fixed incomes, low-income families, and those living in rapidly appreciating areas face significant financial strain. High property taxes can force families to choose between paying their taxes and meeting other essential needs, such as food, healthcare, or childcare. This inequity contributes to social and economic disparities. For example, a comparison of property tax burdens as a percentage of income across different income brackets in Colorado would highlight the regressive nature of the current system. Areas with high concentrations of lower-income households might show significantly higher tax burdens compared to wealthier areas, even if the property values are lower.

Examples of Successful Property Tax Reforms in Other States

Several states have successfully implemented property tax reforms that have addressed affordability and equity concerns. For instance, [State A] reformed its assessment system to provide more predictable and transparent tax calculations, leading to increased property owner satisfaction and reduced litigation. [State B] implemented a circuit breaker program, offering tax relief to low-income seniors and disabled individuals, significantly improving their financial stability. These examples demonstrate that effective reforms are achievable and can lead to positive outcomes. A detailed comparison of these reforms and their impact on property tax burdens, economic growth, and social equity would further strengthen this argument. We can analyze metrics such as homeowner satisfaction surveys, economic growth rates, and income inequality measures before and after implementation.

Hypothetical Property Tax Reform Proposal

A potential reform proposal could incorporate several key elements to address affordability concerns. This could include a reassessment of the current property tax rate, possibly reducing it to a more manageable level for homeowners. A graduated property tax system, where higher-value properties are taxed at a higher rate than lower-value properties, could also be implemented to improve equity. Furthermore, a dedicated fund for property tax relief could be established, providing assistance to low-income seniors and families through direct subsidies or tax credits. This fund could be financed through a combination of increased revenue from other sources and a reallocation of existing state resources. Such a multifaceted approach would offer a comprehensive solution to the current challenges.

Arguments Against Property Tax Reform in Colorado

While many advocate for property tax reform in Colorado, significant counterarguments exist. These concerns stem from potential negative consequences, implementation challenges, and the inherent complexities of balancing competing interests within the state’s diverse economic landscape. Ignoring these potential drawbacks could lead to unintended and undesirable outcomes.

Potential Negative Consequences of Property Tax Reform

Reform proposals, while aiming to improve fairness and equity, could inadvertently create new problems. For example, shifting the tax burden might disproportionately impact certain demographics or geographic areas. A poorly designed reform could lead to increased taxes for some homeowners, potentially forcing them from their homes, particularly those on fixed incomes or in lower-income brackets. This could also destabilize local government budgets, as property taxes are a crucial funding source for schools and other essential services. Furthermore, a sudden shift in property values, triggered by reform, could lead to market volatility and uncertainty for homeowners.

Shifting Tax Burdens and Unintended Impacts on Specific Groups

A major concern is that any change to the property tax system might unintentionally increase the tax burden on certain groups of people. For instance, a shift towards a more progressive system might disproportionately impact higher-value properties, potentially driving up taxes for wealthier homeowners. Conversely, a regressive shift could place an undue burden on lower-income homeowners, who may be less able to absorb increased property taxes. The impact on renters should also be considered, as property tax increases often translate into higher rental costs. The potential for displacement of low-income families and seniors needs careful consideration.

Challenges in Implementing Property Tax Reform

Implementing property tax reform in Colorado faces significant practical hurdles. Accurate and consistent property valuations are crucial for a fair system, but achieving this across the state’s diverse geographical areas is a complex task. This involves updating assessment methods, ensuring equitable application across counties, and addressing potential legal challenges from property owners who disagree with their valuations. Furthermore, obtaining political consensus for significant changes to the tax system is notoriously difficult, often requiring compromises that dilute the intended benefits. The logistical challenges of changing assessment practices and updating tax collection systems should also not be underestimated. The transition period could be costly and disruptive.

Comparison of Reform Approaches and Their Potential Drawbacks

Several reform approaches exist, each with its own set of potential benefits and drawbacks. For example, a shift towards a more progressive system, perhaps incorporating a graduated tax rate based on property value, might address equity concerns but could face political resistance from those who would see their taxes increase. Alternatively, increasing reliance on alternative revenue sources, such as sales taxes or income taxes, could lessen the burden on property owners but might shift the tax burden to other groups and create new issues of equity and fairness. A complete overhaul of the assessment system could improve accuracy but would require substantial investment and time to implement effectively. Each approach carries the risk of unintended consequences, requiring careful analysis and consideration.

Potential Unintended Consequences of Specific Reform Proposals

A list of potential unintended consequences, depending on the specific reform proposal, could include: decreased property values in certain areas; increased tax burdens for specific demographic groups; reduced funding for essential public services; legal challenges and protracted court battles; market volatility in the real estate sector; and increased administrative costs for the government. These are not exhaustive, and the specific consequences would depend on the details of the reform proposal. For instance, a sudden and drastic change in property tax rates could trigger a significant drop in property values, negatively affecting homeowners and the broader economy.

Specific Proposals for Property Tax Reform in Colorado

Source: amazonaws.com

Property tax reform in Colorado is a complex issue with no easy solutions. Numerous proposals have been floated over the years, each aiming to address the perceived inequities and burdens of the current system. These proposals often involve intricate mechanisms and have varying impacts on different property owners, necessitating a careful examination of their strengths and weaknesses. Understanding these proposals is crucial for informed participation in the ongoing debate surrounding Colorado property taxes.

The Gallagher Amendment Repeal and Replacement

The Gallagher Amendment, enacted in 1982, aimed to maintain a roughly equal balance between residential and non-residential property tax burdens. However, it has led to significant issues, including dramatic shifts in tax burdens over time and disproportionate impacts on specific property types. Repealing the Gallagher Amendment is a common starting point for many reform proposals. Replacement proposals typically involve creating a new assessment system, often with a focus on establishing a more stable and equitable tax base. Some proposals suggest a phased-in approach to minimize abrupt changes in tax liabilities. For example, a phased repeal could involve gradually reducing the reliance on the Gallagher Amendment’s formula over several years, allowing taxpayers and local governments time to adjust. This approach would aim to mitigate the potential shock of immediate and significant tax increases or decreases for specific property owners.

- Mechanism: Repeal of the Gallagher Amendment and implementation of a new assessment system, potentially with a phased-in approach.

- Intended Outcome: More stable and equitable property tax distribution across different property types.

- Impact on Property Owners: Varies depending on the specific replacement system. Some homeowners might see tax increases, while others might see decreases. Commercial property owners would likely see changes as well.

Increased Property Tax Exemptions

Another approach to property tax reform focuses on increasing property tax exemptions for certain groups of property owners. This could involve raising the homestead exemption, providing additional exemptions for seniors or veterans, or expanding exemptions for specific types of properties, like agricultural land. Increasing exemptions effectively reduces the taxable value of a property, leading to lower property taxes for those who qualify. However, increasing exemptions can reduce the overall tax base, potentially requiring higher tax rates for remaining properties to maintain the same level of government revenue. This can disproportionately impact property owners who do not qualify for the exemptions.

- Mechanism: Increasing the value of existing exemptions or creating new ones for specific groups of property owners.

- Intended Outcome: Provide tax relief for specific vulnerable populations and potentially stimulate the economy through support for agricultural land.

- Impact on Property Owners: Lower taxes for those who qualify for exemptions; potentially higher taxes for those who do not, due to the need for increased tax rates to compensate for reduced revenue.

Shifting the Tax Burden Towards Commercial Properties

Some proposals advocate for shifting a greater share of the property tax burden towards commercial properties. This could involve adjusting assessment ratios or implementing different tax rates for commercial and residential properties. Proponents argue that commercial properties often have greater capacity to absorb increased tax burdens, while opponents worry about potential negative impacts on economic development and business growth. The impact on residential property owners would depend on the extent of the shift and whether it necessitates adjustments to overall tax rates.

- Mechanism: Adjusting assessment ratios or tax rates to increase the relative tax burden on commercial properties.

- Intended Outcome: Reduce the tax burden on residential property owners.

- Impact on Property Owners: Potentially lower taxes for residential property owners, potentially higher taxes for commercial property owners.

Impact of Property Tax Reform on Different Groups: Colorado Property Tax Reform

Property tax reform in Colorado carries significant implications for various segments of the population, impacting homeowners, renters, businesses, and low-income families differently. The success of any reform hinges on its ability to create a fairer and more equitable system, minimizing negative consequences for vulnerable groups while achieving the intended economic goals. Understanding these potential impacts is crucial for informed policymaking.

Impact on Homeowners

The impact on homeowners depends heavily on the specifics of the reform. A shift towards a more progressive system, for example, might lower taxes for owners of lower-valued homes while increasing them for those with high-value properties. Conversely, a reform focusing on property tax rate reductions could provide broad-based relief, but might disproportionately benefit wealthier homeowners who own more valuable properties. For instance, a statewide reduction in the mill levy could result in substantial savings for owners of luxury homes in Aspen, while providing smaller savings to homeowners in smaller towns. Conversely, a reform that focuses on increasing property tax exemptions for certain classes of homeowners, such as seniors or veterans, would specifically benefit those groups.

Impact on Renters

Renters are indirectly affected by property tax changes. Increased property taxes on landlords often translate to higher rents, placing a greater burden on renters, especially those with lower incomes. Conversely, property tax reductions might lead to lower rents, offering some relief. A hypothetical example: if a reform significantly lowers property taxes on apartment complexes in Denver, landlords might pass on some of those savings through reduced rents, benefiting the city’s numerous renters. However, this isn’t guaranteed, as landlords might choose to increase profits instead.

Impact on Businesses

Businesses, particularly commercial property owners, are significantly affected by property taxes. Higher property taxes can increase operating costs, potentially leading to higher prices for consumers or reduced profitability. Conversely, tax reductions can boost business activity and investment. Consider the impact on small businesses in downtown Boulder. Significant property tax increases could force some to close, impacting jobs and the local economy. Conversely, tax relief could incentivize expansion and hiring.

Impact on Low-Income Families

Low-income families are particularly vulnerable to property tax changes. Increased property taxes, whether directly on their homes or indirectly through increased rents, can strain their budgets and reduce their access to essential resources. Reforms must carefully consider the needs of this population. For example, an increase in property taxes, even a small one, can be a significant burden on a family already struggling to make ends meet in a high-cost area like Denver. Conversely, targeted property tax relief programs for low-income homeowners could significantly improve their financial stability.

Projected Impact by Income Bracket

| Reform Proposal | Low Income (<$40,000) | Middle Income ($40,000-$100,000) | High Income (>$100,000) |

|---|---|---|---|

| Statewide Mill Levy Reduction | Small decrease | Moderate decrease | Significant decrease |

| Increased Exemptions for Low-Income Homeowners | Significant decrease | Small decrease | No change |

| Progressive Property Tax System | Small increase/No change | Small decrease/No change | Significant increase |

Funding Mechanisms for Public Services Post-Reform

Colorado’s current system heavily relies on property taxes to fund essential public services like education, infrastructure, and public safety. This reliance creates inequities, as property values fluctuate significantly across the state, leading to uneven funding for schools and other vital services. Reforming property taxes necessitates exploring alternative funding models to ensure consistent and equitable resource allocation.

Current Funding of Public Services in Colorado

Property taxes form a cornerstone of Colorado’s public service funding. Local governments, particularly school districts, heavily depend on property tax revenue to cover operational costs, teacher salaries, and infrastructure maintenance. While other sources like state grants and sales taxes contribute, property taxes often constitute the largest portion of local government budgets. This dependence creates a system vulnerable to fluctuations in property values and economic downturns, impacting the quality and availability of public services.

Alternative Funding Mechanisms

Several alternative funding mechanisms could supplement or replace property taxes. These include increased reliance on state income tax, a broader sales tax base, and dedicated revenue streams from specific industries. Each option presents unique challenges and benefits.

State Income Tax Increase

Raising the state income tax could generate substantial revenue for public services. This approach offers a more progressive funding model, as higher earners contribute proportionally more. However, it could face political resistance and potentially drive high-income earners out of the state. A phased increase, coupled with targeted tax relief for low-income households, might mitigate this risk. For example, a 1% increase in the state income tax, coupled with a $1000 tax credit for families earning less than $50,000 annually, could provide a balance between revenue generation and social equity.

Expanded Sales Tax Base

Broadening the sales tax base to include currently exempt items, like groceries or certain services, could generate additional revenue. This approach is relatively straightforward to implement but could disproportionately impact low-income households if not carefully designed. A tiered system, exempting essential goods from higher tax rates, or offering rebates to low-income families, could mitigate this concern. For instance, a 1% increase in the sales tax, excluding groceries and essential medicines, coupled with a sales tax rebate program for low-income families, could be a more equitable approach.

Dedicated Revenue Streams

Establishing dedicated revenue streams from specific industries, such as a tax on oil and gas production or a tourism tax, could provide a stable and predictable funding source. This approach is appealing as it targets specific sectors benefiting from public services, but it might be politically challenging to implement and could face legal challenges related to taxation of specific industries. A phased implementation, starting with a smaller tax on oil and gas production, followed by gradual increases based on market conditions and revenue projections, could be a more manageable approach.

Transition Plan

A gradual transition away from a property tax-heavy model requires a phased approach. This could involve gradually increasing alternative revenue streams while simultaneously reducing property tax rates over a defined period (e.g., five to ten years). This would allow local governments time to adjust their budgets and avoid abrupt disruptions to public services. Regular monitoring and evaluation of the transition’s impact on different communities and public services would be crucial.

Visual Representation of Funding Models

The visual representation would be a comparative bar chart. The x-axis would represent different funding sources (Property Tax, State Income Tax, Sales Tax, Other Revenue). The y-axis would represent the percentage of total public service funding. Two sets of bars would be presented: one representing the current funding model, with property tax dominating (e.g., 60%), and another representing the proposed alternative model, where the proportion of property tax is reduced (e.g., 30%) and the other sources (State Income Tax, Sales Tax, and Other Revenue) increase proportionally to make up the difference. Clear labels and data points for each funding source in both models would be included to allow for easy comparison. The chart would clearly illustrate the shift in funding sources from a property tax-dominant model to a more diversified funding model. For instance, the current model might show Property Tax at 60%, Sales Tax at 20%, Income Tax at 15%, and Other at 5%. The proposed alternative could show Property Tax at 30%, Sales Tax at 25%, Income Tax at 30%, and Other at 15%.

Closing Summary

So, is Colorado property tax reform the answer to the state’s fiscal puzzle? The short answer is… it’s complicated. While the current system has its flaws, any significant overhaul carries potential risks. The key lies in finding a balanced approach that addresses affordability concerns without crippling essential public services. This requires thoughtful consideration of alternative funding models, a clear understanding of the potential impacts on different groups, and a willingness to engage in robust public discourse. The road to reform may be long and winding, but the destination – a fairer, more sustainable system – is worth the climb.