Fed rate cuts what should savers do cds high yield accounts – Fed Rate Cuts: What Should Savers Do? CDs? High-yield accounts? The recent Fed rate cuts have sent ripples through the savings world, leaving many wondering how to protect their hard-earned cash. Interest rates are falling, impacting returns on traditional savings vehicles like CDs and high-yield savings accounts. But fear not, savvy saver! This guide navigates the choppy waters of fluctuating interest rates, offering practical strategies to safeguard your savings and even potentially boost your returns.

We’ll break down the mechanics of Fed rate cuts, explore how they affect different savings options, and present alternative strategies to consider. From understanding the risk-reward profiles of various investments to adjusting your long-term financial plans, we’ve got you covered. Get ready to become a rate-cut-resistant savings ninja!

Understanding Fed Rate Cuts

Source: usmodularinc.com

The Federal Reserve (Fed) regularly adjusts interest rates to influence the U.S. economy. Rate cuts, a decrease in the federal funds rate, are a key monetary policy tool used to stimulate economic growth during periods of slowdown or recession. Understanding these cuts, their mechanics, and historical impact is crucial for navigating financial decisions.

The Fed’s primary tool is the federal funds rate—the target rate banks charge each other for overnight lending. When the Fed cuts this rate, it becomes cheaper for banks to borrow money. This lower borrowing cost is then passed on to consumers and businesses through lower interest rates on loans, mortgages, and credit cards. Increased borrowing fuels spending and investment, boosting economic activity. Conversely, higher rates curb borrowing and spending, aiming to control inflation.

The Mechanics of Fed Rate Cuts and Their Impact on the Economy

A Fed rate cut injects liquidity into the financial system. Lower interest rates encourage businesses to invest in expansion projects and hire more employees, leading to job creation and increased consumer confidence. Lower borrowing costs also make it more affordable for consumers to purchase homes, cars, and other big-ticket items, further stimulating economic growth. However, this increased spending can also fuel inflation if it outpaces the economy’s productive capacity. The delicate balance the Fed aims for is stimulating growth without triggering runaway inflation. For example, the significant rate cuts implemented in response to the 2008 financial crisis aimed to prevent a deeper recession, although it also contributed to a period of relatively low inflation afterward.

Historical Correlation Between Fed Rate Cuts and Inflation

The relationship between Fed rate cuts and inflation isn’t always straightforward. While rate cuts are often associated with periods of low inflation, or even deflation, this is not always the case. The impact depends heavily on the economic context. For instance, during periods of economic slowdown, rate cuts may not lead to significant inflation because demand remains subdued. Conversely, if the economy is already operating at full capacity, rate cuts could lead to increased demand and subsequent inflationary pressure. The 1970s provide a stark example; despite several rate cuts, inflation remained stubbornly high due to supply-side shocks and strong demand. Conversely, the rate cuts following the 2008 financial crisis were largely successful in averting deflation, though inflation remained subdued for several years.

Types of Fed Rate Cuts and Their Potential Effects

The Fed doesn’t just cut the federal funds rate; it also influences other rates through various mechanisms. These include changes to the discount rate (the rate at which commercial banks borrow directly from the Fed), reserve requirements (the percentage of deposits banks must hold in reserve), and open market operations (the buying and selling of government securities to influence the money supply). Each of these actions can have slightly different impacts on the economy. For example, a decrease in reserve requirements allows banks to lend more freely, potentially stimulating economic activity more quickly than a simple federal funds rate cut. The specific effects depend on the interplay of various economic factors, and the Fed carefully considers these nuances when implementing monetary policy.

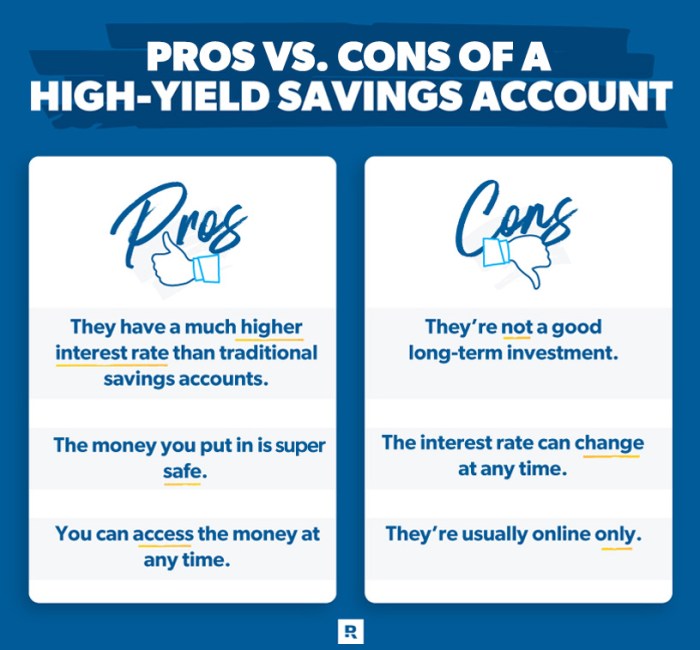

Impact on Savings Accounts: Fed Rate Cuts What Should Savers Do Cds High Yield Accounts

Source: ramseysolutions.net

The Federal Reserve’s decision to cut interest rates directly impacts the returns you see on your savings. While rate cuts are generally good for borrowers, they can mean lower returns for savers who rely on interest income. Understanding how these cuts affect different savings vehicles, like Certificates of Deposit (CDs) and high-yield savings accounts, is crucial for making informed financial decisions.

The relationship between interest rates and savings account yields is straightforward: lower Fed rates generally lead to lower yields. This is because banks base their offered interest rates on the rates they can borrow money at – the federal funds rate being a key benchmark. When the Fed cuts rates, banks have less incentive to offer high yields on savings accounts to attract deposits. However, the impact varies depending on the account type and the magnitude of the rate cut.

Comparison of CD and High-Yield Savings Account Returns

CDs and high-yield savings accounts react differently to interest rate changes. CDs offer fixed interest rates for a specified term, meaning your return is locked in regardless of subsequent rate cuts (though you’ll face penalties for early withdrawal). High-yield savings accounts, on the other hand, typically have variable interest rates that adjust with market conditions, meaning your returns will likely decrease after a rate cut. The extent of the decrease depends on the bank’s pricing strategy and the magnitude of the Fed’s action.

Rate Cut Magnitude and Yield Impacts, Fed rate cuts what should savers do cds high yield accounts

A 0.25% rate cut will usually result in a smaller decrease in yields compared to a 0.5% cut. For example, a high-yield savings account yielding 4% might drop to 3.75% after a 0.25% Fed rate cut, while a 0.5% cut could reduce it to 3.5%. CDs, having fixed rates, would remain unaffected unless the CD matures and is rolled over at a lower rate.

Hypothetical Scenario: $10,000 Investment

Let’s illustrate the impact with a hypothetical scenario. We’ll assume a $10,000 investment in both a CD and a high-yield savings account. For simplicity, we will ignore compounding interest within the short timeframe of the rate cut.

| Account Type | Initial Investment | Rate Cut Scenario | Final Balance (Approximate) |

|---|---|---|---|

| High-Yield Savings Account (Initial Yield: 4%) | $10,000 | 0.25% Rate Cut | $10,375 (Assuming a new yield of 3.75%) |

| High-Yield Savings Account (Initial Yield: 4%) | $10,000 | 0.5% Rate Cut | $10,350 (Assuming a new yield of 3.5%) |

| CD (Fixed Rate: 4%) | $10,000 | 0.25% Rate Cut | $10,400 (Assuming a 4% annual yield) |

| CD (Fixed Rate: 4%) | $10,000 | 0.5% Rate Cut | $10,400 (Assuming a 4% annual yield) |

Alternative Savings Strategies

So, the Fed’s cutting rates. Your high-yield savings account isn’t looking so hot anymore. Don’t panic! There are other avenues to explore for your hard-earned cash, each with its own set of pros and cons. Let’s dive into some alternatives that might offer better returns or more stability in this shifting financial landscape.

Money market accounts, government bonds, and even carefully chosen stocks and bonds (though that requires a different level of risk tolerance and expertise), all offer potential solutions. The key is understanding your risk tolerance and financial goals before making any decisions.

Money Market Accounts

Money market accounts (MMAs) offer a balance between accessibility and slightly higher returns than traditional savings accounts. They typically pay a competitive interest rate, often exceeding that of standard savings accounts, though usually less than high-yield options. However, this higher rate is usually still influenced by the federal funds rate, so while they may outperform savings accounts, the benefit may be lessened during periods of rate cuts. MMAs also usually offer check-writing and debit card capabilities, providing greater flexibility than CDs. The risk is generally low, as MMAs are FDIC-insured up to $250,000 per depositor, per insured bank, for each account ownership category. Tax implications are similar to savings accounts; interest earned is typically taxable as ordinary income.

Government Bonds

Government bonds, issued by the U.S. Treasury, are considered one of the safest investments available. They offer a fixed interest rate (coupon) paid periodically until maturity, and you receive the face value of the bond at maturity. While the interest rate on government bonds might not always outpace inflation, they offer a degree of stability and predictability not found in other investments. The risk is low, although bond prices can fluctuate based on market interest rates. If you sell a bond before maturity, you might experience a loss if interest rates have risen since you purchased the bond. Interest earned on government bonds is generally taxable as ordinary income, although certain types of municipal bonds may offer tax advantages depending on your state and local tax laws. For example, a Series I bond’s interest rate is adjusted twice a year based on inflation, offering a potential hedge against inflation.

Risk-Reward Profiles Compared to CDs and High-Yield Savings Accounts

Let’s compare the risk-reward profiles. High-yield savings accounts and CDs offer relatively low risk and liquidity, but their returns are directly tied to the federal funds rate, making them less attractive during rate cut periods. MMAs offer slightly higher returns with similar liquidity and low risk. Government bonds offer a balance of safety and potential returns, but their liquidity is lower and their returns are fixed. The choice depends on your individual financial goals and risk tolerance. A conservative investor might prefer CDs or MMAs, while someone willing to accept slightly more risk might consider government bonds.

Managing Risk and Volatility

Navigating the choppy waters of fluctuating interest rates requires a keen understanding of your own risk tolerance and a proactive approach to safeguarding your savings. Rate cuts, while potentially beneficial for borrowers, can impact the returns on your savings accounts. This section Artikels strategies to assess your risk profile and mitigate the potential negative effects of these fluctuations.

The key to successful savings management during periods of economic uncertainty lies in understanding your individual circumstances and aligning your investment strategies accordingly. Risk tolerance isn’t a fixed trait; it’s a dynamic assessment based on your financial goals, time horizon, and overall comfort level with potential losses.

Assessing Risk Tolerance

Understanding your risk tolerance is crucial before making any significant financial decisions. Consider your financial goals: are you saving for a short-term purchase (like a car) or a long-term goal (like retirement)? Short-term goals generally require a more conservative approach, prioritizing capital preservation over high returns. Long-term goals allow for a higher risk tolerance, as you have more time to recover from potential losses. Your time horizon directly influences your risk tolerance. A longer time horizon provides more opportunities to ride out market downturns and recover from losses. For example, someone saving for retirement in 30 years can tolerate more risk than someone saving for a down payment on a house in 2 years. Finally, your overall comfort level with potential losses is a key factor. Are you comfortable with the possibility of seeing your savings fluctuate in value? Honest self-assessment in these areas is paramount.

Strategies to Mitigate the Impact of Rate Cuts

Several strategies can help mitigate the impact of rate cuts on your savings. Diversification is key: don’t put all your eggs in one basket. Spread your savings across different account types, such as high-yield savings accounts, CDs, and money market accounts, to reduce your overall risk. Staggered investments help to average out the impact of fluctuating interest rates. Instead of investing a large sum at once, invest smaller amounts over time. This approach, known as dollar-cost averaging, reduces the risk of investing a large sum at a market low.

- Diversify your savings: Spread your money across different accounts with varying levels of risk and return.

- Employ dollar-cost averaging: Invest smaller amounts regularly to mitigate the impact of market fluctuations.

- Consider inflation-protected securities: These investments aim to maintain purchasing power even during periods of inflation.

Strategies to Maintain Savings Goals During Economic Uncertainty

Maintaining your savings goals during periods of economic uncertainty requires a proactive and adaptable approach. Regularly review your budget and identify areas where you can cut expenses. This might involve temporarily reducing discretionary spending or finding more affordable alternatives for essential goods and services. Consider increasing your savings rate if possible. Even small increases can make a significant difference over time. Finally, stay informed about economic trends and adjust your savings strategy as needed. Don’t be afraid to seek professional financial advice if you feel overwhelmed or unsure about how to proceed.

- Budgeting and Expense Reduction: Identify non-essential expenses to cut back on.

- Increased Savings Rate: Allocate a larger portion of your income to savings.

- Financial Education and Professional Advice: Stay informed and seek expert guidance when needed.

Long-Term Savings Planning

Navigating Fed rate cuts requires a proactive approach to your long-term savings strategy. While lower rates might seem initially discouraging for savers, they present an opportunity to re-evaluate and potentially optimize your financial plan for the long haul. Understanding the implications and making timely adjustments can significantly impact your future financial security.

Adjusting your long-term financial plan in response to anticipated Fed rate cuts involves a strategic, multi-step process. It’s not about panic, but about informed decision-making based on a clear understanding of your goals and the shifting economic landscape.

Adjusting Retirement Savings Plans

The impact of Fed rate cuts on retirement savings can be significant, particularly for those relying on interest income. Lower rates mean less return on fixed-income investments like CDs and savings accounts. However, this also presents opportunities to adjust your investment strategy to maximize growth potential. For example, if you’re nearing retirement and heavily invested in low-yield instruments, you might consider shifting a portion of your portfolio to higher-growth investments like equities (stocks) to offset the lower returns from fixed-income investments, although this carries higher risk. Conversely, if you are still many years away from retirement, you might use the opportunity to invest more aggressively, knowing that you have more time to recover from potential market downturns.

Step-by-Step Guide to Adjusting Long-Term Savings Plans

A methodical approach is crucial when adapting your long-term savings plan to changing interest rate environments. Consider these steps:

- Review Your Current Financial Situation: Assess your current assets, liabilities, and income. Determine your risk tolerance and time horizon for your savings goals. This provides a baseline for informed decisions.

- Re-evaluate Investment Portfolio Allocation: Analyze the performance of your current investments. Consider diversifying your portfolio to minimize risk. This might involve shifting some assets from low-yield instruments to higher-growth investments, or vice-versa, depending on your risk tolerance and time horizon.

- Adjust Savings Contributions: If your income allows, consider increasing your savings contributions to compensate for lower returns on fixed-income investments. This helps you stay on track with your long-term financial goals.

- Explore Alternative Investment Options: Explore alternative investment options like index funds, ETFs, or real estate. Remember that these options come with varying degrees of risk and require careful consideration.

- Regularly Review and Adjust: Economic conditions are dynamic. Regularly review your financial plan (at least annually, or more frequently during periods of significant economic change) and make adjustments as needed to ensure you remain on track to achieve your financial goals. This proactive approach helps to mitigate the impact of unexpected market fluctuations.

Example: Adjusting Retirement Savings Plan

Let’s say Sarah, age 50, is nearing retirement and has a significant portion of her retirement savings in CDs. With anticipated Fed rate cuts, the returns on her CDs will decrease. To mitigate this, Sarah might consider gradually shifting a portion of her CD investments into a diversified portfolio of stocks and bonds, balancing risk and return based on her time horizon and risk tolerance. She could consult a financial advisor to create a personalized strategy. Alternatively, John, age 30, with a longer time horizon, might choose to increase his contributions to his retirement account, taking advantage of potentially lower valuations in the market and aiming for long-term growth.

Importance of Regular Review and Adjustment

Regularly reviewing and adjusting your savings strategies is paramount. Economic conditions, interest rates, and personal circumstances can change unexpectedly. A static plan may not adapt effectively to these changes, potentially jeopardizing your long-term financial goals. Proactive monitoring and adjustment ensure that your savings plan remains aligned with your goals and risk tolerance throughout your life. Ignoring these changes can lead to missed opportunities or increased risk.

Illustrative Example: Impact on Retirement Savings

Source: sputnikglobe.com

Let’s examine how a series of Fed rate cuts can significantly affect a retiree’s income stream, particularly when relying heavily on savings accounts and CDs for their retirement funds. We’ll explore a hypothetical scenario to illustrate the potential consequences and highlight the need for adaptable retirement strategies.

Imagine Sarah, a 65-year-old retiree, who has $500,000 in savings, primarily distributed between a high-yield savings account and CDs. Her annual income relies heavily on the interest generated from these accounts. Before the rate cuts, she earned a comfortable, albeit modest, income from the interest.

Retirement Income Under Varying Rate Cut Scenarios

This section details Sarah’s income and savings over a five-year period under different rate cut scenarios. We will assume three scenarios: Scenario A (no rate cuts, interest rates remain stable at 3%), Scenario B (moderate rate cuts resulting in a gradual decline in interest rates to 1% over five years), and Scenario C (aggressive rate cuts, reducing interest rates to 0.5% over the same period).

Scenario A (Stable Rates): Sarah’s initial annual interest income is $15,000 ($500,000 x 0.03). This remains consistent throughout the five-year period. Her account balance grows modestly due to compounding interest, reaching approximately $579,637 after five years. A visual representation would show a steadily increasing line graph.

Scenario B (Moderate Rate Cuts): In the first year, Sarah earns $15,000. However, interest rates gradually decrease. By year five, her annual income drops to $5,000 ($500,000 x 0.01), reflecting the cumulative impact of the rate cuts. The account balance graph would show a slower growth curve compared to Scenario A, gradually flattening. The final balance after five years would be approximately $525,000.

Scenario C (Aggressive Rate Cuts): This scenario presents a more challenging picture. Sarah’s annual income shrinks more dramatically, starting at $15,000 and falling to $2,500 by year five ($500,000 x 0.005). The visual representation would display a nearly flat line graph, reflecting minimal growth. Her final balance after five years would be approximately $512,500.

Implications for Retirement Planning and Adjustment Strategies

The scenarios clearly demonstrate how vulnerable retirees relying on interest income can be to Fed rate cuts. Scenario C, in particular, illustrates a significant reduction in income, potentially jeopardizing Sarah’s retirement lifestyle.

To mitigate such risks, retirees should diversify their income sources beyond savings accounts and CDs. This could include exploring options like: annuities, which provide a guaranteed stream of income; investments in dividend-paying stocks or bonds, offering a potentially higher return (although with greater risk); and part-time work or consulting, supplementing their retirement income. Regularly reviewing and adjusting the retirement plan based on economic conditions is crucial. This might involve shifting assets to higher-yielding instruments (when available) or exploring other income-generating avenues. Professional financial advice can prove invaluable in navigating such complexities and building a more resilient retirement plan.

Last Recap

Navigating the impact of Fed rate cuts on your savings requires a proactive approach. While lower interest rates might seem daunting, they also present opportunities for strategic adjustments. By understanding the mechanics of rate cuts, diversifying your savings portfolio, and regularly reviewing your long-term financial plan, you can weather the storm and continue building your financial future. Remember, staying informed and adaptable is key to successful saving in any economic climate. So, grab your financial planner, analyze your options, and get ready to make your money work smarter, not harder!